April 7th, 2026

Choosing between a fixed-rate and an adjustable-rate mortgage (ARM) is a crucial decision that depends on your financial situation, long-term plans, and risk tolerance.

Choosing between a fixed-rate and an adjustable-rate mortgage is like selecting the perfect dance partner for your home financing journey.

With a fixed-rate mortgage, where your payments waltz steadily to a predictable rhythm, providing unwavering stability as you glide through the years.

On the other hand, envision the thrill of an adjustable-rate mortgage, where you start with a dynamic, lower rate and embrace the potential for future savings as market rhythms change.

Whether you seek the comforting embrace of consistency or the possibility of lower initial costs, understanding the unique strengths of each can help you decide on a mortgage strategy that perfectly aligns with your financial aspirations and lifestyle.

Here’s a breakdown of the key differences and factors to consider to help you determine which type of mortgage might be right for you:

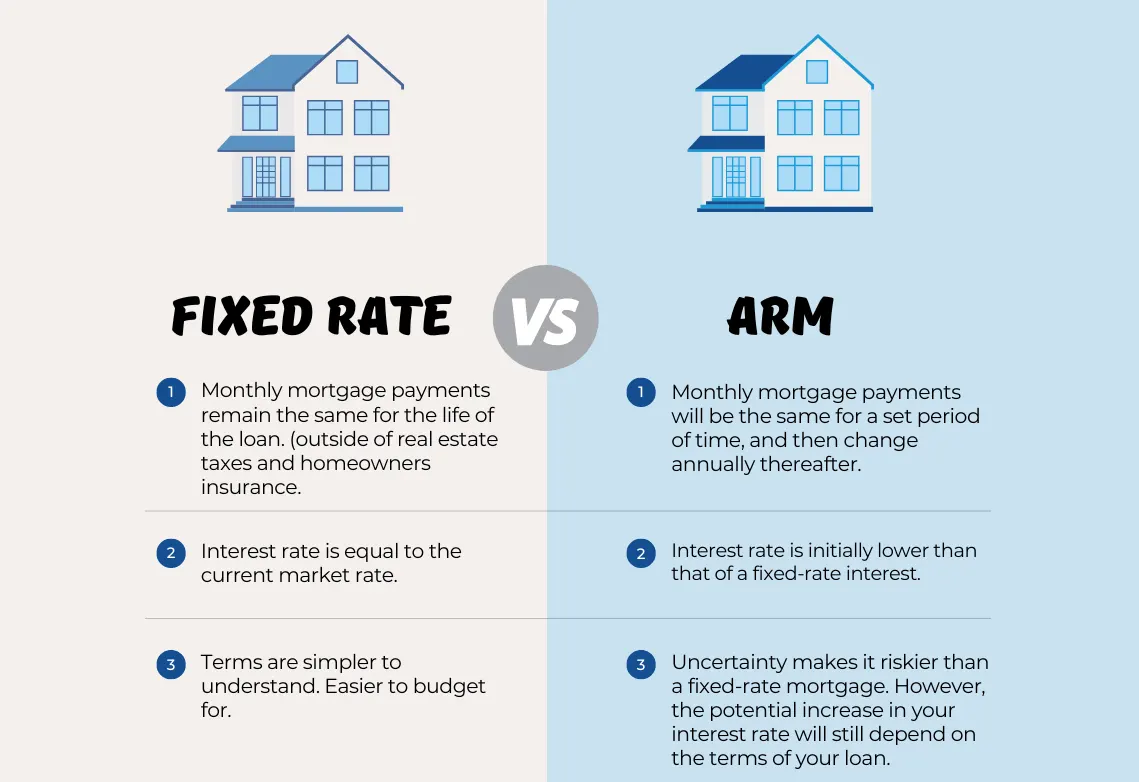

Fixed-Rate Mortgages

Overview:

- Stability: Fixed-rate mortgages have an interest rate that remains constant throughout the life of the loan. This means your monthly payments are predictable and won’t change over time.

- Term Lengths: Common fixed-rate terms are 15, 20, or 30 years, though other variations exist.

- Interest Rates: Typically, fixed-rate mortgages have slightly higher interest rates compared to ARMs, but they offer long-term stability.

Pros:

- Predictability: Monthly payments remain consistent, making it easier to budget and plan for the future.

- Protection Against Rate Increases: You’re protected from market fluctuations and rising interest rates.

- Simplicity: Easier to understand and manage due to its straightforward nature.

Cons:

- Higher Initial Rates: The initial interest rate is usually higher than the starting rate of an ARM, potentially leading to higher monthly payments initially.

- Less Flexibility: If market rates decrease, you’re locked into your higher rate unless you refinance.

Best For:

- Long-Term Homeowners: If you plan to stay in your home for a long time and value stability, a fixed-rate mortgage might be the best option.

- Budget-Conscious Borrowers: If you prefer predictable payments and a steady budget, a fixed-rate mortgage offers peace of mind.

Adjustable-Rate Mortgages (ARMs)

Overview:

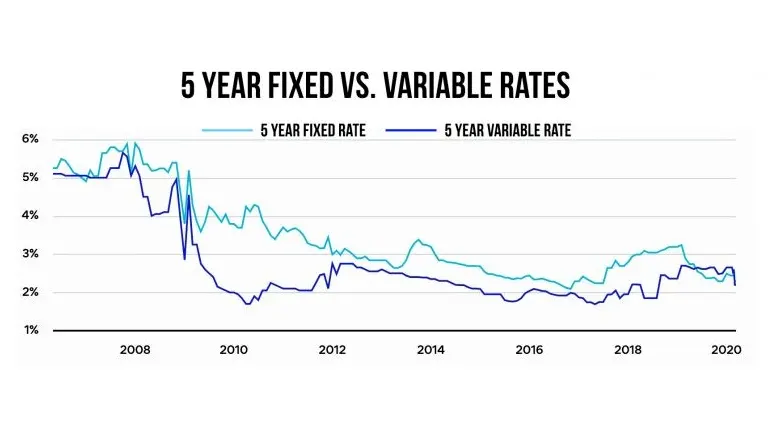

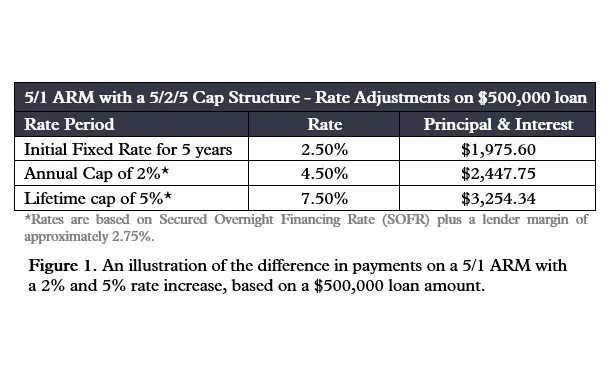

- Variable Rates: ARMs have interest rates that can fluctuate based on market conditions. They typically start with a lower initial rate that is fixed for a specific period (e.g., 5, 7, or 10 years), after which the rate adjusts periodically based on an index.

- Initial Rate Period: Common ARMs include 5/1, 7/1, or 10/1 ARMs, where the first number indicates the fixed-rate period and the second number indicates how often the rate adjusts afterward.

Pros:

- Lower Initial Rates: ARMs often offer lower initial interest rates compared to fixed-rate mortgages, which can result in lower monthly payments at the start.

- Potential Savings: If interest rates remain stable or decrease, you could benefit from lower payments over time compared to a fixed-rate mortgage.

Cons:

- Payment Uncertainty: Monthly payments can vary after the initial fixed-rate period, making budgeting more challenging.

- Risk of Rate Increases: There’s a risk that interest rates—and consequently your payments—could increase significantly after the initial period.

- Complexity: ARMs can be more complex due to terms like adjustment periods, caps, and margins.

Best For:

- Short-Term Homeowners: If you plan to move or refinance before the adjustable period begins, an ARM could save you money with its lower initial rates.

- Risk-Tolerant Borrowers: If you can handle potential payment fluctuations and are comfortable with market risks, an ARM might be appealing.

Factors to Consider When Choosing:

- Time Horizon: How long do you plan to stay in your home? If you’re staying long-term, a fixed-rate mortgage provides stability. For shorter stays, an ARM with a lower initial rate might be more cost-effective.

- Financial Stability: Assess your comfort with potential payment fluctuations. If you prefer consistent payments, a fixed-rate mortgage offers peace of mind.

- Current Interest Rates: Evaluate the current interest rate environment. If rates are high, an ARM with a lower initial rate might be advantageous, but consider potential future rate increases.

- Budget Flexibility: Determine how flexible your budget is. If you can handle potential increases in monthly payments, an ARM could be a viable option.

- Risk Tolerance: Consider your willingness to take on the risk of changing rates. Fixed-rate mortgages offer security, while ARMs offer potential savings with some risk.

Ultimately, the right choice depends on your personal financial situation, future plans, and comfort with risk. Carefully weigh the benefits and drawbacks of each type of mortgage and consider consulting a financial advisor or mortgage specialist to help make the best decision for your needs.

Best Market Conditions to choose Fixed-Rate vs. Adjustable-Rate Mortgages

Choosing between a fixed-rate and adjustable-rate mortgage (ARM) depends significantly on the prevailing market conditions and your personal financial situation. Here’s a guide to the best market conditions for each type of mortgage:

Best Market Conditions for Fixed-Rate Mortgages

- Low Interest Rates:

- Why: When interest rates are low, locking in a fixed-rate mortgage can be advantageous because you secure a low rate for the entire term of the loan. This can save you money over the life of the loan compared to ARMs, which might have higher initial rates.

- Action: Consider a fixed-rate mortgage to take advantage of the current low rates and ensure stability in your payments.

- Stable or Rising Interest Rates:

- Why: If interest rates are expected to rise or remain stable, a fixed-rate mortgage can provide protection against future rate increases. You’ll benefit from predictable payments and avoid the risk of paying higher rates later.

- Action: Opt for a fixed-rate mortgage to lock in a rate before potential increases, especially if you plan to stay in your home long-term.

- Long-Term Homeownership:

- Why: If you plan to stay in your home for many years, a fixed-rate mortgage offers the advantage of stable payments throughout the loan term, regardless of market fluctuations.

- Action: Choose a fixed-rate mortgage to ensure long-term financial stability and budget predictability.

Best Market Conditions for Adjustable-Rate Mortgages (ARMs)

- High Initial Rates with Declining or Stable Rates:

- Why: When fixed rates are high but are expected to decline or remain stable, an ARM with a lower initial rate can provide significant savings. You benefit from lower payments initially and potentially lower rates if market conditions improve.

- Action: Consider an ARM if you anticipate that overall interest rates will decrease or stabilize, and you’re comfortable with potential future adjustments.

- Short-Term Homeownership:

- Why: If you plan to move or refinance before the initial fixed-rate period of the ARM ends, you can take advantage of the lower initial rates without worrying about future rate adjustments.

- Action: Opt for an ARM if you expect to sell or refinance within the initial fixed period, allowing you to capitalize on lower rates without facing long-term variability.

- Favorable Adjustment Caps:

- Why: Some ARMs come with caps that limit how much the interest rate can increase during each adjustment period or over the life of the loan. In a market where rates are expected to fluctuate but not rise dramatically, these caps can provide a safety net.

- Action: Choose an ARM with favorable adjustment caps if you’re willing to accept some rate variability but want protection against excessive increases.

- Improving Credit Profile:

- Why: If you expect your credit score to improve, you might be able to refinance into a better loan or obtain a more favorable ARM rate later on. An ARM could be a strategic choice if you anticipate better financial conditions in the near future.

- Action: Consider an ARM if you anticipate significant improvements in your credit profile that could lead to better refinancing opportunities.

Additional Considerations:

- Economic Indicators: Pay attention to economic indicators such as inflation rates, central bank policies, and overall economic stability. These can provide insights into future interest rate trends.

- Personal Financial Situation: Consider your financial stability, risk tolerance, and future plans. Your comfort with payment variability and long-term financial goals should guide your decision.

By aligning your mortgage choice with current market conditions and your personal circumstances, you can make an informed decision that maximizes your financial benefits and suits your homeownership goals.

When considering fixed-rate and adjustable-rate mortgages (ARMs), choosing the right lender can make a significant difference in terms of rates, fees, and customer service.

Here are some top lenders for each type of mortgage:

Top Lenders for Fixed-Rate Mortgages

- Quicken Loans (Rocket Mortgage)

- Why: Quicken Loans, now known as Rocket Mortgage, is renowned for its streamlined application process and competitive fixed-rate mortgage options. They offer a wide range of term lengths and provide excellent customer service.

- Wells Fargo

- Why: Wells Fargo provides a variety of fixed-rate mortgage options with competitive rates. They offer personalized service and a range of resources to help first-time homebuyers and experienced borrowers alike.

- Chase

- Why: Chase offers competitive fixed-rate mortgages with flexible terms. They have a strong reputation for customer service and a variety of online tools to help manage your mortgage.

- Bank of America

- Why: Bank of America provides fixed-rate mortgages with various term options and competitive rates. They also offer tools and resources for mortgage management and homebuyer education.

- USAA

- Why: USAA offers fixed-rate mortgages with competitive rates, particularly for military members and their families. They are known for their specialized service and understanding of the unique needs of military families.

Top Lenders for Adjustable-Rate Mortgages (ARMs)

- LendingTree

- Why: LendingTree is an online marketplace that allows you to compare ARM offers from multiple lenders. They provide access to a range of lenders with competitive ARM rates and terms.

- PenFed Credit Union

- Why: PenFed offers attractive ARM options with competitive initial rates and favorable terms. They are known for their low fees and good customer service, particularly for members.

- Citi

- Why: Citi provides a variety of ARM products with competitive rates and flexible terms. They offer tools to help you understand and manage your ARM, as well as a solid reputation for customer service.

- BB&T (now Truist)

- Why: BB&T, now Truist, offers a range of ARM options with competitive rates and flexible adjustment periods. They provide personalized service and a variety of mortgage resources.

- New American Funding

- Why: New American Funding offers competitive ARM rates with various fixed-rate periods and adjustment options. They are known for their customer service and range of mortgage products.

Factors to Consider When Choosing a Lender:

- Interest Rates: Compare the initial rates and adjustment terms of ARMs or the fixed rates and terms of fixed-rate mortgages.

- Fees and Closing Costs: Evaluate the fees and closing costs associated with the loan to understand the overall cost.

- Customer Service: Look for lenders with strong customer service and support throughout the mortgage process.

- Flexibility: Consider the flexibility of loan terms, such as the ability to make extra payments or refinance without penalties.

- Online Tools: Utilize online tools and calculators offered by lenders to assess your mortgage options and manage your loan.

Choosing the right lender involves more than just comparing rates. It’s important to consider the overall value of the loan, including customer service, fees, and the lender’s reputation.

--- article sharing ---