July 28th, 2026

Understanding the differences between fixed, variable, and introductory interest rates is crucial for making informed borrowing decisions.

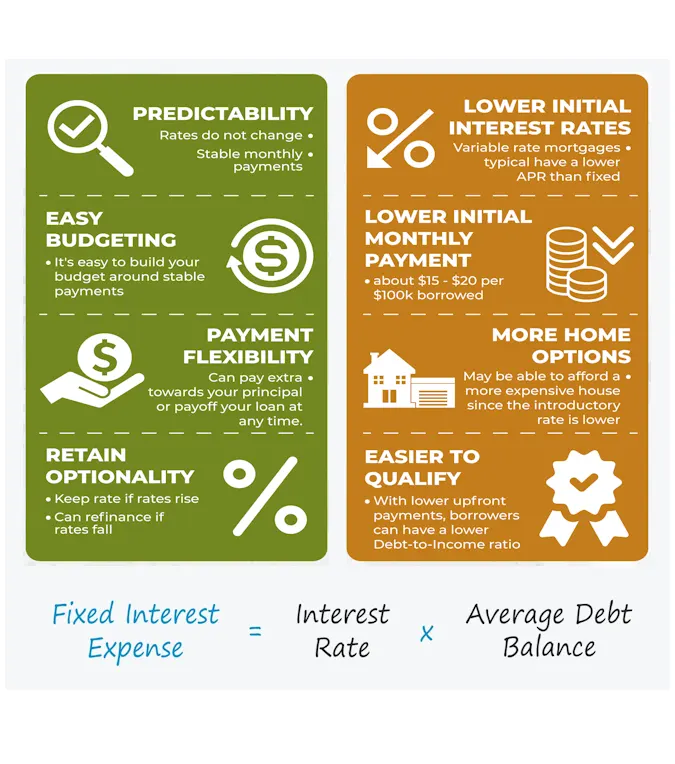

Fixed interest rates remain constant throughout the loan term, providing predictable monthly payments and stability, which is ideal for long-term planning.

Variable interest rates, on the other hand, fluctuate based on market conditions and are often tied to an index like the prime rate.

While they can start lower than fixed rates, they carry the risk of increasing over time, potentially raising your monthly payments.

Introductory offers typically feature low or even 0% interest rates for an initial period, making them attractive for short-term borrowing or balance transfers.

However, it’s important to be aware of the terms, as rates can significantly increase after the introductory period ends.

Carefully evaluating these options and considering your financial situation and risk tolerance can help you choose the most suitable interest rate type for your needs.

About Interest Rates: Fixed, Variable, and Introductory Offers

Understanding interest rates is crucial when managing loans and credit, as they directly affect the cost of borrowing and your monthly payments.

When navigating the world of borrowing, understanding the different types of interest rates—fixed, variable, and introductory offers—is crucial to making informed financial decisions.

Fixed interest rates provide stability and predictability, as they remain constant throughout the life of the loan or credit agreement.

This means your monthly payments won’t fluctuate, regardless of changes in market interest rates.

For instance, if you secure a 30-year mortgage with a fixed rate of 4.00%, you can budget confidently knowing your payment amount will remain steady over the entire term.

This can be particularly beneficial in a rising interest rate environment, where future rates could be higher than your fixed rate.

Here’s a detailed breakdown of the different types of interest rates—fixed, variable, and introductory offers—along with what you should know about each:

1. Fixed Interest Rates

Definition:

- A fixed interest rate remains constant throughout the life of the loan or credit agreement. This means that your interest rate and monthly payments will not change, regardless of market conditions.

Advantages:

- Predictability: With a fixed interest rate, you know exactly what your monthly payments will be for the duration of the loan. This makes budgeting easier and provides financial stability.

- Protection from Rate Increases: If interest rates rise, your fixed rate ensures that your payments remain unchanged. This can be particularly advantageous in a rising interest rate environment.

Disadvantages:

- Potentially Higher Initial Rates: Fixed interest rates may start higher than introductory variable rates, meaning you could pay more initially compared to a lower variable rate offer.

Example: A 30-year mortgage with a fixed interest rate of 4.00% ensures that your monthly mortgage payment will remain the same throughout the loan term, providing stability and predictability.

2. Variable Interest Rates

Definition:

- A variable interest rate fluctuates based on changes in an underlying index or benchmark rate, such as the LIBOR (London Interbank Offered Rate) or the prime rate. The rate adjusts periodically, which can lead to changes in your monthly payments.

Advantages:

- Potentially Lower Initial Rates: Variable rates often start lower than fixed rates, which can result in lower initial monthly payments.

- Benefit from Rate Drops: If market interest rates decrease, your variable rate and monthly payments may also decrease, potentially reducing your overall borrowing costs.

Disadvantages:

- Payment Uncertainty: Since rates can increase, your monthly payments might rise over time, making it harder to budget and potentially increasing the total cost of the loan.

- Risk of Rate Increases: If interest rates rise significantly, your payments could become unaffordable, leading to financial strain.

Example: A 5-year adjustable-rate mortgage (ARM) might offer an initial rate of 3.00% for the first five years, after which the rate adjusts annually based on market conditions.

If interest rates rise, your payments could increase significantly after the initial period.

3. Introductory Offers

Definition:

- Introductory offers typically involve promotional interest rates that are lower than standard rates for a specified period at the beginning of the loan or credit agreement. After the introductory period ends, the rate usually adjusts to a higher standard rate.

Advantages:

- Initial Savings: Introductory offers can provide substantial savings during the promotional period, resulting in lower monthly payments and reduced interest costs initially.

- Attractive for Short-Term Needs: If you plan to repay the loan or transfer the balance before the introductory period ends, you can benefit from the lower rate without worrying about the higher rate that follows.

Disadvantages:

- Rate Adjustment: Once the introductory period expires, the interest rate typically increases to the standard or variable rate, which could significantly raise your payments.

- Potential Fees: Some introductory offers come with fees, such as balance transfer fees or annual fees, that might offset the initial savings.

Example: A credit card offering a 0% APR on balance transfers for the first 12 months allows you to pay off existing debt without accruing interest during that period.

After 12 months, the rate might revert to a higher standard APR, such as 15.00%, which could increase your monthly payments if you carry a balance.

Considerations:

When choosing between fixed, variable, or introductory rates, consider your financial situation, how long you plan to keep the loan or credit, and your ability to manage payment fluctuations.

Variable interest rates are tied to an underlying index, such as the LIBOR or the prime rate, and can change periodically based on market conditions.

While variable rates often start lower than fixed rates, they carry the risk of increasing over time, which can lead to higher monthly payments and overall borrowing costs.

For example, a 5-year adjustable-rate mortgage (ARM) might offer an initial rate of 3.00% for the first five years, but after this period, the rate could adjust annually based on current market conditions.

If interest rates rise, your payments will increase accordingly, potentially straining your budget if you’re not prepared for such fluctuations.

Fixed rates offer stability, variable rates might provide lower initial costs but with risk, and introductory offers can save money initially but may lead to higher costs later.

Evaluating these factors will help you select the most suitable option for your needs.

Secrets offered by insider industry experts regarding Interest Rates: Fixed, Variable, and Introductory Offers

Insider industry experts offer several lesser-known tips and strategies for navigating fixed, variable, and introductory interest rates effectively. Understanding these nuances can help you make more informed financial decisions and optimize your borrowing strategy.

1. Fixed Interest Rates: Locking In and Refinancing Opportunities

Secret: While fixed interest rates offer stability, industry insiders suggest that borrowers should actively monitor market conditions for potential refinancing opportunities. If market rates drop significantly, refinancing your existing loan at a lower fixed rate can lead to substantial savings over the life of the loan.

Implementation: Regularly review interest rate trends and consider refinancing if you can secure a lower fixed rate than your current one. Keep an eye on refinancing offers from various lenders and be prepared to act when rates are favorable.

Example: If you have a 30-year mortgage with a fixed rate of 4.50% and market rates drop to 3.75%, refinancing to the lower rate could reduce your monthly payments and save you thousands in interest over the life of the loan.

2. Variable Interest Rates: Managing Risk and Timing

Secret: To mitigate the risks associated with variable interest rates, industry experts recommend setting up a budget that includes a buffer for potential rate increases. Additionally, if your loan or credit account offers the option to convert to a fixed rate, consider this conversion if you anticipate rising rates or plan to keep the loan for an extended period.

Implementation: Calculate the maximum possible payment increase based on historical rate changes and include this in your financial planning. If your lender allows, convert your variable rate to a fixed rate to lock in current rates and avoid future payment spikes.

Example: If you have an adjustable-rate mortgage with a current rate of 3.00%, but you anticipate potential rate hikes, budgeting for payments at 5.00% or higher can prevent financial strain. Converting to a fixed rate when your loan offers this option can provide long-term stability.

3. Introductory Offers: Strategic Use and Avoiding Pitfalls

Secret: Introductory offers can provide significant initial savings, but industry insiders advise careful management of these offers to avoid pitfalls.

To maximize the benefit, ensure you understand the terms and plan to pay off balances or transfer them before the introductory period ends.

Additionally, be aware of potential fees that might offset the initial savings.

Implementation: Set reminders for the end of the introductory period and develop a strategy to pay off the balance or transfer it to another low-rate option before the promotional rate expires.

Review all terms associated with the offer, including any balance transfer fees or annual fees.

Example: If a credit card offers 0% APR on balance transfers for the first 12 months, plan to pay off or significantly reduce the balance before the promotional period ends.

Also, check for balance transfer fees that might reduce the overall savings from the introductory offer.

By leveraging these insider strategies—monitoring refinancing opportunities for fixed rates, budgeting for potential increases with variable rates, and managing introductory offers strategically—you can make the most of different interest rate structures and optimize your financial outcomes.

Dirty Little Secrets of Interest Rates: Fixed, Variable, and Introductory Offers

When it comes to interest rates, there are several “dirty little secrets” that industry insiders rarely disclose but are crucial for understanding the true cost of borrowing. These secrets can reveal potential pitfalls and strategies to navigate the complexities of fixed, variable, and introductory rates effectively.

1. Fixed Interest Rates: Hidden Costs and Market Timing

Secret: One hidden cost associated with fixed interest rates is the potential for overpaying if you lock in a rate that is higher than current market rates. Lenders often emphasize the stability and predictability of fixed rates, but they may not disclose how market conditions can fluctuate. If you lock in a fixed rate during a period of high interest rates, you could end up paying more over the life of your loan than if you waited for rates to drop or refinanced later.

Implementation: Stay informed about current market rates and economic forecasts. Use online tools and financial calculators to compare potential savings from refinancing or waiting for a more favorable rate. Don’t assume a fixed rate is always the best option without evaluating market trends.

Example: If you secure a fixed-rate mortgage at 5.00% during a period of high rates, but rates drop to 3.50% a year later, you could have missed out on significant savings by not waiting or refinancing.

2. Variable Interest Rates: Unseen Risks and Rate Caps

Secret: A major hidden risk of variable interest rates is the potential for sharp increases due to changes in the underlying index or benchmark.

While variable rates often start lower than fixed rates, they are susceptible to significant increases if the index they are tied to rises.

Additionally, many variable-rate loans have a cap on how much the rate can increase per adjustment period, but these caps can still lead to substantial long-term costs if rates rise significantly.

Implementation: Understand the terms of your variable rate agreement, including the index it’s tied to, the frequency of adjustments, and any caps on rate increases.

Regularly monitor interest rate trends and the performance of the index to anticipate potential changes in your payments.

Example: If you have a 5/1 ARM with an initial rate of 3.00% that adjusts annually, and the index rises significantly, your rate could increase sharply after the initial period, potentially making your payments unaffordable even if there is an annual cap on rate increases.

3. Introductory Offers: Hidden Fees and Payment Shock

Secret: Introductory offers often come with hidden fees and conditions that can negate the benefits of the lower initial rates.

For credit cards, there may be balance transfer fees, annual fees, or high-interest rates that apply after the introductory period ends.

Additionally, if you don’t manage the balance effectively, you may experience payment shock when the rate reverts to a higher standard rate.

Implementation: Thoroughly review all terms and fees associated with an introductory offer.

Plan ahead to pay off or transfer balances before the introductory period ends, and be aware of the standard rate and any fees that apply once the promotional period concludes.

Example: A credit card with 0% APR on balance transfers for the first 12 months might charge a 3% balance transfer fee.

If you don’t pay off the balance within the introductory period, you could face a high APR of 18.00% after the 12 months, leading to unexpected financial strain.

Understanding these “dirty little secrets” can help you navigate the complexities of interest rates more effectively.

By staying informed about market conditions, understanding the full terms of your loan or credit agreement, and planning strategically for changes, you can better manage the costs associated with borrowing and avoid potential pitfalls.

Lenders that offer the best Interest Rates: Fixed, Variable, and Introductory Offers

When looking for the best interest rates, it’s important to consider lenders that offer competitive options for fixed, variable, and introductory rates.

Here’s a breakdown of some top lenders known for providing attractive interest rates across these categories:

1. Fixed Interest Rates

1. Quicken Loans (Rocket Mortgage)

- Overview: Quicken Loans, now operating under the name Rocket Mortgage, is renowned for offering competitive fixed interest rates for various types of loans, including mortgages and personal loans.

- Why They’re Top: They offer a range of fixed-rate mortgage options with transparent pricing and no hidden fees. Their online platform makes it easy to compare rates and secure a fixed rate.

- Example: A 30-year fixed mortgage might be available at rates as low as 3.00% depending on your credit profile and market conditions.

2. US Bank

- Overview: US Bank provides attractive fixed interest rates for both mortgages and personal loans.

- Why They’re Top: Known for competitive rates and comprehensive customer service, US Bank offers various fixed-rate loan products with flexible terms.

- Example: A 15-year fixed mortgage might come with rates starting around 2.75%, providing a lower total cost over the life of the loan compared to a 30-year fixed rate.

2. Variable Interest Rates

1. Chase

- Overview: Chase offers competitive variable interest rates on a range of products including credit cards and adjustable-rate mortgages (ARMs).

- Why They’re Top: Chase’s variable rates are often lower at the start compared to fixed rates, and they offer several options for adjusting rates based on market conditions.

- Example: A 5/1 ARM might start at an initial rate of 2.75%, with annual adjustments based on current market indices.

2. Bank of America

- Overview: Bank of America provides variable interest rates for both credit cards and adjustable-rate home loans.

- Why They’re Top: Their variable rates are competitive, and they offer a range of products with transparent terms and conditions.

- Example: An adjustable-rate mortgage might feature an initial rate of 3.00%, with adjustments tied to the LIBOR or SOFR index after the initial period.

3. Introductory Offers

1. Discover

- Overview: Discover offers attractive introductory APRs on their credit cards, including balance transfers and new purchases.

- Why They’re Top: They often provide 0% APR on balance transfers and purchases for an extended introductory period, making them ideal for short-term borrowing or consolidating debt.

- Example: Discover’s credit cards might offer 0% APR on balance transfers for 18 months, followed by a standard APR of around 15.99% to 22.99% depending on creditworthiness.

2. Citi

- Overview: Citi provides compelling introductory offers on several credit cards, including 0% APR periods for both balance transfers and new purchases.

- Why They’re Top: Citi’s credit cards often feature long introductory periods and valuable rewards, making them a strong choice for those looking to manage or consolidate debt.

- Example: The Citi Double Cash Card offers 0% APR on balance transfers for the first 18 months and then reverts to a variable APR of 18.24% to 28.24%.

Conclusion

When evaluating lenders for the best interest rates, consider both the current market conditions and your specific financial needs.

Fixed-rate options from lenders like Quicken Loans and US Bank offer stability, while Chase and Bank of America provide competitive variable rates.

For those seeking introductory offers, Discover and Citi stand out with attractive promotional rates.

Always compare multiple lenders, review the terms and fees associated with each option, and choose the one that best aligns with your financial goals and borrowing needs.

--- article sharing ---