July 25th, 2026

Loan amortization is the process of paying off a loan through regular, scheduled payments that cover both principal and interest.

Each payment is divided into two parts: the interest due on the outstanding loan balance and the principal repayment.

Initially, a larger portion of your payment goes towards interest, but as the loan matures, more of your payment is applied to the principal.

This gradual shift is detailed in an amortization schedule, which outlines each payment’s breakdown over the loan term.

Understanding this process can help you see how extra payments can reduce your principal faster, saving you money on interest in the long run.

Using tools like amortization calculators or spreadsheet software can provide a clear picture of your loan’s progression and help you make informed financial decisions.

If you’re considering a loan, reviewing the amortization schedule can give you insights into the true cost of borrowing and help you plan your finances more effectively.

Loan Amortization: How Your Payments are Calculated

Loan amortization is a fundamental concept in borrowing that determines how your loan payments are calculated and how your loan balance decreases over time.

Understanding amortization can help you manage your debt more effectively and make informed financial decisions.

Here’s a detailed explanation of loan amortization and how your payments are calculated:

1. What is Loan Amortization?

Loan amortization refers to the process of paying off a loan over time through scheduled, periodic payments. Each payment consists of both principal and interest.

Initially, a larger portion of each payment goes toward interest, while a smaller portion reduces the principal balance.

Over time, as the principal balance decreases, the interest portion of each payment decreases, and the principal portion increases.

This gradual shift ensures that the loan is fully repaid by the end of the term.

Example: For a 30-year fixed-rate mortgage, your monthly payments are structured so that you’ll pay off the entire loan balance by the end of the 30-year period.

Early payments will primarily cover interest costs, while later payments will contribute more to reducing the principal.

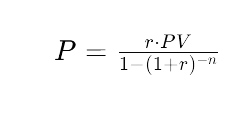

2. How Are Payments Calculated?

Loan amortization is a systematic process that outlines how your loan payments are structured to ensure that the loan is fully paid off by the end of its term.

Understanding amortization is crucial for managing loans effectively, as it helps you comprehend how each payment contributes to reducing the loan balance and how interest costs accumulate over time.

The calculation of loan payments involves determining how much you need to pay each period to fully repay the loan by the end of its term.

This involves using the following formula:

where:

- P = Monthly payment

- r = Monthly interest rate (annual rate divided by 12)

- PV = Present value or principal amount of the loan

- n = Total number of payments (loan term in months)

Example: For a $200,000 mortgage with a 4% annual interest rate over 30 years, you’d divide the annual rate by 12 to get a monthly interest rate of approximately 0.00333.

Plugging these numbers into the formula calculates your fixed monthly payment, which covers both principal and interest.

This formula determines how much you need to pay each month to fully amortize the loan by the end of its term.

It ensures that your payments are sufficient to cover both interest and principal over the agreed period.

Example: For a $200,000 loan with a 5% annual interest rate over 15 years, you would divide the annual rate by 12 to get a monthly interest rate of approximately 0.00417.

Plugging these numbers into the formula calculates your fixed monthly payment. For this example, the monthly payment would be approximately $1,582, which covers both interest and principal.

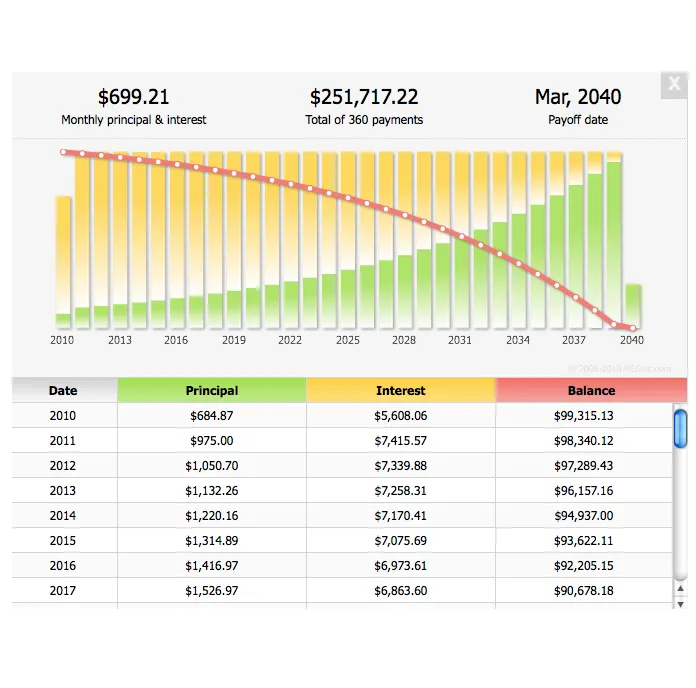

3. Understanding the Amortization Schedule

An amortization schedule is a detailed table showing each payment’s breakdown into principal and interest components, as well as the remaining balance after each payment.

This schedule helps you see how your payments will be allocated over the life of the loan and how much of each payment is reducing the principal versus paying interest.

Example: In the first month of a mortgage, the payment might include $800 toward interest and $200 toward the principal.

By the 10th year, the payment structure will reverse, with a larger portion going toward the principal and less toward interest.

The amortization schedule will illustrate this gradual change, providing transparency on how each payment impacts your loan balance.

Understanding loan amortization is crucial for managing your finances effectively.

Amortization can be looked at as the gradual repayment of a loan through regular payments that cover both principal and interest.

At the start of the loan, a larger portion of each payment goes toward interest, while a smaller portion reduces the principal balance.

Over time, as the principal decreases, the interest portion of each payment also decreases, and more of each payment goes toward reducing the principal.

This structure ensures that the loan is repaid in full by the end of the term.

Example: For a 30-year fixed-rate mortgage of $300,000 at a 4% annual interest rate, the monthly payment is calculated using the amortization formula, which includes both principal and interest.

In the early years of the loan, your payment might primarily cover the interest costs, with only a small fraction reducing the principal.

As time progresses, the principal reduction portion increases, and the interest portion decreases.

By knowing how payments are structured, you can better plan for the future, make informed decisions about refinancing or extra payments, and understand how interest and principal payments affect your overall loan costs.

Secrets offered by insider industry experts regarding Loan Amortization

Industry insiders have several “secrets” about loan amortization that can provide valuable insights for managing your loans more effectively and avoiding common pitfalls.

Here’s what you should know about how your payments are calculated and what to watch out for:

1. The Impact of Early Payments

Secret: Making extra payments or paying more than the minimum amount due can significantly reduce the total interest paid over the life of the loan and shorten the loan term.

This is because additional payments go directly toward reducing the principal balance, which lowers the amount of interest charged in subsequent periods.

Implementation: If you make an extra payment each month, or even just make an additional annual payment, you can substantially reduce the total interest expense and pay off the loan earlier.

Some loans also offer the option to make bi-weekly payments instead of monthly payments, which effectively results in an extra payment each year.

Example: On a 30-year mortgage of $300,000 with a 4% interest rate, making an extra $100 payment each month can shave several years off the loan term and save thousands in interest over the life of the loan.

2. Understanding the Effect of Interest Rates on Amortization

Secret: The interest rate on your loan has a profound impact on your amortization schedule. A small increase in the interest rate can significantly increase your total payments over the life of the loan.

Conversely, securing a lower interest rate can dramatically reduce your total cost.

Implementation: Always consider how changes in interest rates might affect your loan. If you’re offered a lower interest rate, it’s often worth refinancing to lock in those savings.

Conversely, if rates are expected to rise, locking in a fixed rate before the increase could save money.

Example: For a $200,000 loan with a 3.5% interest rate, the total payment over 30 years might be around $327,000. If the rate increases to 4.5%, the total payment could rise to over $360,000, demonstrating the substantial impact of interest rate changes.

3. Watch Out for Prepayment Penalties and Hidden Fees

Secret: Some loans come with prepayment penalties or hidden fees that can negate the benefits of paying off your loan early or making additional payments.

These penalties can be significant and are often not well-publicized at the time of loan origination.

Implementation: Before committing to a loan, carefully review the terms and conditions related to prepayment.

Ask the lender explicitly if there are any penalties or fees associated with paying off the loan early or making extra payments. Factor these potential costs into your decision-making process.

Example: A mortgage with a $10,000 prepayment penalty might render making extra payments or paying off the loan early less attractive.

If the penalty outweighs the interest savings from early repayment, it might be better to stick with the regular payment schedule.

4. The Benefit of Re-amortizing Your Loan

Secret: Re-amortizing, or re-calculating the amortization schedule, can be beneficial if you make a lump-sum payment toward the principal.

This process adjusts your monthly payment to reflect the reduced balance, potentially lowering your payments for the remaining term of the loan.

Implementation: Check with your lender about the option to re-amortize your loan after making a large principal payment. This can help reduce your monthly payments and overall interest costs.

Example: If you receive a bonus and apply it as a lump-sum payment to your mortgage principal, re-amortizing the loan might lower your monthly payments, providing you with immediate financial relief.

Consideration

Understanding these insider tips can help you manage your loan more effectively, optimize your payments, and avoid common financial pitfalls.

By leveraging extra payments, monitoring interest rates, being aware of prepayment penalties, and considering re-amortization, you can better control your borrowing costs and make more strategic financial decisions.

Lenders that offer the best loans considering amortization and payment terms beneficial to borrowers

When selecting a lender, it’s crucial to consider how their loan products align with your financial goals, particularly in terms of amortization and payment terms.

Here are some top lenders known for offering favorable loan terms, including flexible amortization schedules, beneficial payment structures, and competitive interest rates:

1. Quicken Loans (Rocket Mortgage)

Overview: Quicken Loans, now operating under Rocket Mortgage, is known for its user-friendly platform and competitive loan terms. They offer a variety of mortgage products with flexible amortization schedules.

Why They’re Top:

- Flexible Terms: Offers a range of fixed and adjustable-rate mortgages with various term lengths, allowing you to choose a schedule that fits your financial situation.

- Online Tools: Provides an easy-to-use online calculator to help you understand your amortization schedule and monthly payments.

- Customer Service: Known for excellent customer service and support throughout the loan process.

Example: Rocket Mortgage offers 15, 20, and 30-year fixed-rate mortgages with competitive rates and customizable payment options, helping borrowers manage their amortization schedules effectively.

2. US Bank

Overview: US Bank provides various mortgage and personal loan options with beneficial amortization terms. They are well-regarded for their transparency and competitive rates.

Why They’re Top:

- Customizable Loans: Offers both fixed and adjustable-rate mortgages with flexible amortization schedules, including options for bi-weekly payments.

- Amortization Calculators: Provides tools to help you plan your payments and see how extra payments can impact your loan term.

- Loan Products: Includes options such as 30-year and 15-year fixed mortgages, as well as adjustable-rate mortgages with favorable terms.

Example: A 30-year fixed mortgage with US Bank allows for a stable payment schedule with the option to make additional payments to reduce the overall loan term.

3. Chase

Overview: Chase offers a variety of mortgage and home equity products with competitive rates and flexible terms. They are known for their comprehensive loan options and customer service.

Why They’re Top:

- Flexible Amortization: Provides various term lengths and payment options, including adjustable-rate mortgages with competitive introductory rates.

- Online Resources: Offers tools and resources to help borrowers understand amortization and manage their loan payments effectively.

- Customer Support: Known for strong customer support and a streamlined application process.

Example: Chase’s 5/1 ARM provides a lower initial rate with the flexibility of adjusting rates periodically after the initial five-year period, allowing for potentially lower payments.

4. Bank of America

Overview: Bank of America is a major lender offering a range of mortgage and home equity products with competitive terms and flexible amortization options.

Why They’re Top:

- Wide Range of Products: Includes fixed-rate and adjustable-rate mortgages with various term lengths, providing options for different financial needs.

- Amortization Tools: Offers calculators and tools to help you plan and manage your loan payments effectively.

- Competitive Rates: Provides competitive rates and terms, making it easier for borrowers to find favorable amortization schedules.

Example: Bank of America’s 30-year fixed mortgage offers stable monthly payments and the option to make additional payments to reduce the total interest paid.

5. Wells Fargo

Overview: Wells Fargo provides various loan products with flexible amortization options, including fixed and adjustable-rate mortgages. They are known for their extensive branch network and customer service.

Why They’re Top:

- Flexible Terms: Offers multiple term lengths and payment structures, including options for bi-weekly payments and additional principal payments.

- Amortization Support: Provides tools to help borrowers understand their payment schedules and how additional payments can affect their loans.

- Customer Focus: Known for personalized service and support throughout the loan process.

Example: Wells Fargo’s 15-year fixed-rate mortgage allows for higher monthly payments but significantly reduces the overall interest paid compared to a 30-year term.

6. Navy Federal Credit Union

Overview: Navy Federal Credit Union offers competitive loan products with favorable terms for eligible military members and their families. They are known for their member-focused approach.

Why They’re Top:

- Member Benefits: Provides various fixed and adjustable-rate mortgages with competitive rates and flexible amortization schedules.

- Financial Tools: Offers resources and tools to help members manage their loans and amortization effectively.

- Customer Service: Highly rated for excellent customer service and support.

Example: Navy Federal offers a 30-year fixed-rate mortgage with the option for bi-weekly payments, which can help members pay off their loans faster.

7. PNC Bank

Overview: PNC Bank provides a range of mortgage and personal loan products with competitive rates and flexible terms, making it a strong choice for borrowers.

Why They’re Top:

- Flexible Payment Options: Offers various mortgage terms and the option for bi-weekly payments or additional principal payments.

- Amortization Calculators: Provides tools to help you plan your payments and understand your amortization schedule.

- Customer Support: Known for good customer service and a range of loan products tailored to different needs.

Example: PNC’s fixed-rate mortgages come with various term lengths and payment options, including the ability to make additional payments to reduce the loan term.

8. Citibank

Overview: Citibank offers a variety of loan products with competitive rates and flexible amortization terms. They are known for their global presence and financial services.

Why They’re Top:

- Range of Products: Includes both fixed and adjustable-rate mortgages with flexible term lengths and payment options.

- Online Tools: Provides calculators and resources to help borrowers understand and manage their amortization schedules.

- Customer Experience: Known for good customer service and a streamlined application process.

Example: Citibank offers 20-year fixed-rate mortgages, which can be a good middle ground between the longer-term 30-year mortgages and shorter-term 15-year options.

9. SunTrust (now Truist)

Overview: SunTrust, now operating as Truist, offers competitive mortgage and personal loan products with favorable terms and flexible payment options.

Why They’re Top:

- Flexible Terms: Provides various term lengths and payment options, including adjustable-rate mortgages with competitive rates.

- Amortization Tools: Offers resources to help you manage your payments and amortization schedule effectively.

- Customer Support: Known for strong customer service and a range of loan products.

Example: Truist’s 10/1 ARM provides a lower initial rate with a longer adjustment period, offering a balance between initial savings and payment stability.

10. HSBC

Overview: HSBC offers competitive mortgage products with flexible terms and payment options, suitable for both domestic and international borrowers.

Why They’re Top:

- Global Reach: Provides various loan products with competitive rates, benefiting from its international network.

- Flexible Amortization: Offers multiple term lengths and the option for bi-weekly payments or additional principal payments.

- Customer Experience: Known for good customer service and comprehensive loan options.

Example: HSBC’s fixed-rate mortgages come with various term options and competitive rates, allowing borrowers to choose an amortization schedule that fits their financial goals.

When choosing a lender, it’s essential to consider how their loan products align with your financial goals, particularly regarding amortization and payment terms.

Lenders like Quicken Loans, US Bank, Chase, and HSBC offer flexible and competitive loan options.

By reviewing the terms, using available tools, and understanding your needs, you can select a lender that provides the best loan terms for your situation.

Amortization Schedule

An amortization schedule is a detailed table that shows how each payment is divided between interest and principal, as well as the remaining loan balance after each payment.

This schedule helps borrowers understand how their payments affect the loan balance over time and provides insight into the total interest paid throughout the loan term.

Example: In the first month of a 30-year mortgage, the amortization schedule might show that $1,000 of your $1,432 payment goes toward interest, while $432 reduces the principal.

As you make payments, the schedule will reflect a gradual increase in the principal portion of each payment and a decrease in the interest portion.

By the 10th year, the majority of your payment will be applied to the principal, and the interest portion will be much lower.

Understanding loan amortization and how payments are calculated can help you manage your debt more effectively.

By knowing how each payment affects your loan balance and interest costs, you can make informed decisions about additional payments, refinancing, or adjusting your loan term to better meet your financial goals.

--- article sharing ---