August 4th, 2026

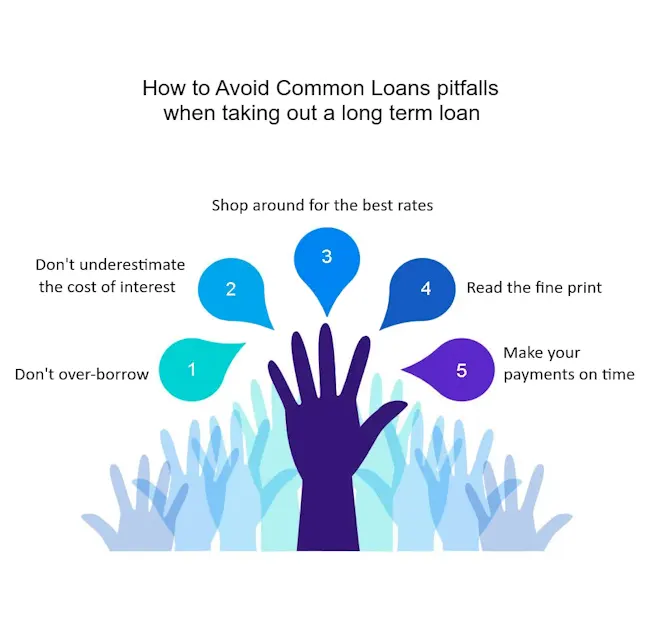

When taking out a personal loan, it’s essential to avoid common pitfalls to ensure you don’t end up paying more than necessary.

First, always check your credit score before applying, as this will influence your interest rate and loan terms.

For example, improving your credit score from 600 to 700 could significantly lower your interest rate, saving you hundreds of dollars over the loan term.

Next, shop around and compare offers from multiple lenders to find the best rates and lowest fees.

Avoid borrowing more than you need; while it might be tempting to take out a larger loan, this will increase your monthly payments and the total interest paid.

For instance, borrowing $10,000 instead of $8,000 could cost you an extra $500 in interest over three years.

Finally, ensure you understand all fees associated with the loan, such as origination fees or prepayment penalties, and have a solid repayment plan to avoid late payments and additional charges.

Taking these steps can help you secure a loan that fits your financial situation without unnecessary costs.

Things To Avoid When Taking Out a Personal Loan

Taking out a personal loan can be a strategic way to manage expenses or consolidate debt, but it’s essential to navigate the process carefully to avoid common pitfalls.

Here’s a detailed guide on how to avoid these pitfalls and ensure you get the most out of your personal loan:

1. Understand the Total Cost of the Loan

Pitfall: One of the most significant pitfalls when taking out a personal loan is not fully understanding the total cost of borrowing.

Many borrowers focus solely on the monthly payment and overlook the total amount paid over the life of the loan, including interest and fees.

Avoidance Strategy: Before committing to a loan, calculate the total cost of borrowing by considering the interest rate, loan term, and any additional fees.

Use a loan calculator to estimate your total payments over the life of the loan. Make sure to compare these costs across different lenders to ensure you’re getting the best deal.

Example: A $10,000 personal loan with a 10% interest rate over 5 years might have a total repayment amount of approximately $12,735, including interest.

Understanding this total cost helps you gauge whether the loan is financially viable.

2. Check for Fees and Penalties

Pitfall: Some personal loans come with hidden fees, such as origination fees, prepayment penalties, or late fees, which can significantly increase the cost of the loan or reduce its benefits.

Avoidance Strategy: Carefully review the loan agreement for any fees or penalties. Ask the lender about all potential costs, including origination fees, annual fees, prepayment penalties, and late fees.

Ensure you understand how these fees might impact the overall cost of the loan and your ability to pay it off early if you choose to.

Example: An origination fee of 3% on a $10,000 loan adds $300 to the total cost.

If the loan also has a prepayment penalty, this could offset any savings you might gain by paying off the loan early.

3. Evaluate Your Ability to Repay

Pitfall: Borrowers often overestimate their ability to repay a loan, leading to financial strain or default. It’s crucial to assess your financial situation realistically before taking on new debt.

Avoidance Strategy: Conduct a thorough review of your budget and monthly expenses to determine how much you can comfortably afford to pay each month.

Factor in any other existing debt obligations and ensure that taking on a new loan will not jeopardize your financial stability.

Use a debt-to-income ratio calculator to gauge your ability to handle additional debt.

Example: If your monthly income is $4,000 and you have $1,500 in existing debt payments, ensure that the new loan payment will fit within your remaining $2,500 budget.

Overextending yourself could lead to missed payments and damage to your credit score.

4. Choose the Right Loan Type

Pitfall: Selecting the wrong type of loan for your needs can lead to higher costs or less favorable terms.

Personal loans can vary widely in terms of interest rates, repayment periods, and loan types (secured vs. unsecured).

Avoidance Strategy: Match the loan type to your financial needs and credit profile. Unsecured loans may have higher interest rates but don’t require collateral.

Secured loans might offer lower rates but involve risking an asset. Choose the type of loan that aligns with your risk tolerance and financial situation.

Example: If you have strong credit and don’t have assets to offer as collateral, an unsecured personal loan might be more suitable despite a higher rate compared to a secured loan that requires collateral but offers a lower rate.

5. Watch for Predatory Lenders

Pitfall: Predatory lenders may offer seemingly attractive terms but include exploitative practices such as exorbitant fees, high-interest rates, and unfavorable loan terms.

Avoidance Strategy: Research lenders thoroughly and look for reviews or complaints from other borrowers.

Verify that the lender is reputable and offers transparent terms.

Check for accreditation with organizations like the Better Business Bureau (BBB) and ensure that the lender complies with state and federal regulations.

Example: A lender offering a personal loan with an interest rate significantly higher than average and numerous fees may be engaging in predatory practices.

Avoid such lenders by comparing rates and terms with reputable institutions.

Consideration:

Avoiding common pitfalls when taking out a personal loan involves a thorough understanding of the loan’s total cost, careful consideration of fees and penalties, realistic assessment of your repayment ability, choosing the right loan type, and steering clear of predatory lenders.

By following these strategies, you can secure a personal loan that meets your needs without jeopardizing your financial well-being.

Lenders that help you avoid Common Pitfalls When Taking Out a Personal Loan

When looking for lenders who can help you avoid common pitfalls associated with personal loans, it’s essential to choose those known for transparency, fair practices, and customer support.

Here are some reputable lenders that stand out for their commitment to helping borrowers navigate the personal loan process effectively:

1. SoFi

Overview: SoFi is known for its borrower-friendly approach, including competitive rates, no fees, and flexible terms. They offer personal loans with a focus on transparency and customer support.

Why They’re Top:

- No Fees: SoFi charges no origination fees, prepayment penalties, or late fees, which helps you avoid additional costs.

- Flexible Terms: Offers a range of loan amounts and repayment terms, allowing you to choose an option that fits your financial situation.

- Customer Support: Provides robust customer support and financial advice, including tools to help you understand the total cost of borrowing.

Example: If you take out a $15,000 loan with SoFi, you’ll have no hidden fees and will benefit from clear, upfront terms, helping you avoid unexpected costs.

2. Marcus by Goldman Sachs

Overview: Marcus offers personal loans with no fees and competitive interest rates. Their straightforward terms and transparent fee structure make them a strong choice for borrowers.

Why They’re Top:

- No Fees: Marcus charges no origination fees, late fees, or prepayment penalties, reducing the risk of additional charges.

- Flexible Repayment: Offers flexible repayment options and terms ranging from 36 to 72 months.

- Clear Terms: Provides a clear breakdown of loan terms and payment schedules, helping you understand the total cost of borrowing.

Example: Marcus’s $10,000 loan with a 6% interest rate would have no additional fees, making it easier to manage the cost and avoid common pitfalls.

3. Discover Personal Loans

Overview: Discover provides personal loans with competitive rates, no fees, and a straightforward application process. They are known for their transparency and customer service.

Why They’re Top:

- No Fees: Discover charges no origination fees, late fees, or prepayment penalties.

- Flexible Terms: Offers loans with terms ranging from 36 to 84 months, allowing for manageable monthly payments.

- Easy Application: Provides a transparent application process with clear explanations of terms and conditions.

Example: With Discover, you can take out a $20,000 loan with no hidden fees, allowing you to focus on repayment without worrying about additional costs.

4. LightStream (a division of SunTrust Bank)

Overview: LightStream offers personal loans with competitive rates and a focus on borrower satisfaction. They are known for their flexibility and transparent fee structure.

Why They’re Top:

- No Fees: LightStream charges no fees, including no prepayment penalties, which helps you avoid extra costs.

- Rate Beat Program: Offers a rate beat program where they may offer a lower rate if you find a better rate elsewhere.

- Flexible Terms: Provides flexible loan terms and amounts, with a focus on customer satisfaction and clarity.

Example: If you secure a $30,000 loan through LightStream, you benefit from no additional fees and the possibility of a lower rate through their rate beat program.

5. American Express Personal Loans

Overview: American Express offers personal loans with transparent terms and no fees. Their customer-focused approach helps borrowers manage their loans effectively.

Why They’re Top:

- No Fees: American Express does not charge origination fees, late fees, or prepayment penalties.

- Competitive Rates: Provides competitive interest rates and flexible loan terms.

- Customer Service: Known for high-quality customer service and clear communication regarding loan terms and conditions.

Example: An American Express personal loan of $12,000 would have no hidden fees, ensuring that you know the total cost of borrowing from the outset.

6. Avant

Overview: Avant specializes in personal loans for borrowers with varying credit profiles and offers clear terms with no hidden fees.

Why They’re Top:

- Transparent Terms: Offers loans with clear, upfront terms and no hidden fees.

- Credit Flexibility: Provides options for borrowers with less-than-perfect credit, with a focus on transparent communication.

- Customer Support: Provides helpful customer support and tools to understand loan costs.

Example: With Avant, a $8,000 loan with a moderate interest rate would come with clear terms and no surprise fees, helping you manage your loan effectively.

7. Credible

Overview: Credible is a loan marketplace that allows you to compare personal loan offers from various lenders. They provide a platform that helps you find loans with transparent terms and no hidden fees.

Why They’re Top:

- Comparison Tool: Offers a comparison tool to evaluate loan terms and rates from multiple lenders in one place.

- No Fees: The platform helps you find lenders that charge no fees or prepayment penalties.

- Transparency: Provides clear information on loan terms and costs from various lenders.

Example: By using Credible, you can compare offers for a $25,000 loan and choose the lender that provides the best terms with no hidden fees.

8. LendingClub

Overview: LendingClub offers personal loans with competitive rates and a focus on transparent, borrower-friendly terms. They provide options for both good and fair credit profiles.

Why They’re Top:

- No Hidden Fees: Offers loans with no prepayment penalties and transparent fee structures.

- Flexible Terms: Provides a range of loan amounts and terms, with clear information on costs.

- Customer Service: Known for good customer support and transparent communication about loan terms.

Example: A $5,000 loan from LendingClub would have no prepayment penalties and clear terms, helping you avoid unexpected costs.

9. Upgrade

Overview: Upgrade provides personal loans with a focus on transparency and flexibility, offering competitive rates and no fees.

Why They’re Top:

- No Fees: Charges no origination fees, late fees, or prepayment penalties.

- Flexible Terms: Offers a range of loan amounts and terms to suit different needs.

- Transparency: Provides clear explanations of loan terms and costs, helping you understand the total borrowing cost.

Example: An Upgrade loan of $7,000 would come with straightforward terms and no hidden fees, making it easier to manage your repayments.

10. Earnest

Overview: Earnest is known for its flexible and transparent personal loan options, catering to a variety of borrower needs with clear terms and no fees.

Why They’re Top:

- No Fees: Offers loans with no origination fees, late fees, or prepayment penalties.

- Customizable Loans: Provides customizable loan terms and amounts to fit your financial situation.

- Clear Communication: Ensures transparent communication about loan terms and costs.

Example: With Earnest, a $15,000 personal loan would be offered with no hidden fees and customizable terms, helping you avoid common pitfalls.

Things to Consider

Choosing the right lender is crucial for managing personal loans effectively. Lenders like SoFi, Marcus by Goldman Sachs, and Discover offer transparent terms, no hidden fees, and flexible repayment options, making it easier to avoid common pitfalls and manage your loan responsibly.

By selecting a lender with these qualities, you can navigate the borrowing process with confidence and minimize the risk of unexpected costs.

Secrets offered by industry insiders regarding how to avoid pitfalls when taking out a personal loan

When taking out a personal loan, avoiding common pitfalls and ensuring you get the best deal involves a mix of strategic planning and thorough research. Here’s insider advice and secrets from industry experts on how to navigate the loan landscape effectively:

1. Thoroughly Research and Compare Lenders

Expert Insight: One of the most critical steps in securing a favorable personal loan is researching and comparing multiple lenders. Industry experts emphasize that borrowers should not settle for the first offer they receive. Instead, they should compare offers from a range of lenders to ensure they get the most competitive terms.

Strategy: Use online comparison tools and marketplaces to gather quotes from different lenders. Pay attention to the Annual Percentage Rate (APR), which includes both the interest rate and any fees associated with the loan. The APR provides a more comprehensive view of the loan’s cost than the nominal interest rate alone.

Example: If Lender A offers a personal loan with a 6% interest rate but charges a 5% origination fee, and Lender B offers a 7% interest rate with no fees, calculating the APR will reveal that Lender A might be more expensive overall. Comparing APRs helps ensure you choose the most cost-effective loan.

2. Beware of Introductory Offers and Promotional Rates

Expert Insight: Promotional or introductory rates can be enticing but often come with hidden drawbacks. These rates may be lower initially but can increase significantly after the introductory period ends. Industry insiders advise that borrowers should understand what happens after the promotional period and how it affects the total loan cost.

Strategy: When evaluating promotional rates, scrutinize the terms of the loan after the introductory period ends. Look for information on how and when the rate will adjust, and calculate the potential impact on your monthly payments and overall loan cost.

Example: A loan with an initial 0% APR for the first 12 months that adjusts to 15% thereafter might seem appealing, but it could result in significantly higher payments after the promotional period ends. Understanding the full impact helps avoid surprises and manage long-term costs effectively.

3. Evaluate the True Cost of the Loan

Expert Insight: It’s crucial to look beyond the monthly payment and assess the total cost of the loan over its entire term. Experts recommend calculating how much you will pay in total, including interest and any fees, to avoid loans that may appear attractive but are costly in the long run.

Strategy: Use loan calculators to project the total amount you will pay over the life of the loan. Include all associated fees, such as origination fees, prepayment penalties, and late fees. Compare these costs across different loans to find the most economical option.

Example: A $10,000 loan with a 7% interest rate over 5 years might have a total cost of around $11,800, while another lender might offer a loan at a 6% interest rate with no fees, resulting in a total cost of around $11,400. The difference in total cost can be significant, especially with larger loan amounts or longer terms.

4. Assess Your Repayment Ability and Loan Terms

Expert Insight: Industry experts stress the importance of evaluating your ability to repay the loan based on your current financial situation. A loan that stretches your budget too thin can lead to missed payments and financial stress. Choose a loan term and monthly payment that align with your budget and long-term financial goals.

Strategy: Create a detailed budget to determine how much you can afford to pay each month without compromising other financial obligations. Consider loan terms that offer manageable payments and ensure you are comfortable with the repayment schedule.

Example: If your monthly budget allows for a $300 loan payment, avoid loans with higher payments or shorter terms that could strain your finances. Opt for a loan with a longer term if it provides a lower monthly payment, but be mindful of the total interest cost.

5. Be Cautious of Lenders with Aggressive Sales Tactics

Expert Insight: Some lenders use aggressive sales tactics to push loans that may not be in your best interest. Experts advise being cautious of lenders who emphasize quick approvals or offer terms that seem too good to be true.

Strategy: Research the lender’s reputation and read reviews from other borrowers. Avoid lenders who pressure you into making quick decisions or who offer terms without providing full details. Look for lenders with transparent terms and a strong track record of customer service.

Example: If a lender is offering a personal loan with an unusually low interest rate but requires you to sign immediately, take the time to review the terms carefully and compare with other offers. Ensure you understand all aspects of the loan before committing.

Conclusion

Avoiding common pitfalls when taking out a personal loan requires diligent research, careful evaluation of loan terms, and a clear understanding of the total cost.

By comparing offers, scrutinizing promotional rates, assessing your repayment ability, and avoiding aggressive sales tactics, you can make an informed decision and secure a loan that fits your financial needs.

This approach ensures that you avoid surprises and manage your debt effectively over the long term.