August 1st, 2026

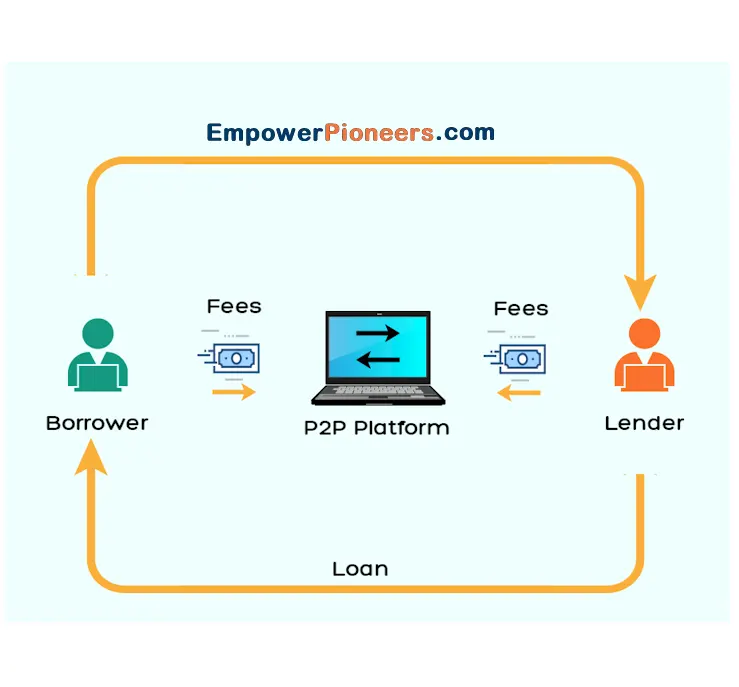

Peer-to-peer (P2P) lending is a method of borrowing and lending that connects individuals or businesses directly with investors through online platforms, bypassing traditional financial intermediaries like banks. Here’s a step-by-step overview of how P2P lending works:

1. Platform Setup and Registration

- Platform Creation: A P2P lending platform, such as LendingClub or Prosper, is established to facilitate connections between borrowers and investors. These platforms typically operate online, making them accessible to a broad audience.

- User Registration: Both borrowers and investors must create accounts on the platform. Borrowers provide information about their financial situation and loan needs, while investors provide details about their investment preferences.

2. Loan Application

- Borrower Application: Borrowers submit an application detailing their loan request, including the amount needed, purpose of the loan, and personal financial information. The application may include a credit check and other assessments.

- Credit Assessment: The platform evaluates the borrower’s creditworthiness using traditional credit scores and alternative data (such as payment history, income, and debt-to-income ratio). Some platforms use proprietary algorithms for risk assessment.

3. Loan Listing

- Loan Listing: Once approved, the loan request is listed on the platform for investors to review. The listing typically includes details about the loan amount, interest rate, term, and the borrower’s credit profile.

- Investment Opportunities: Investors browse available loan listings and choose loans to fund based on their risk tolerance and investment criteria.

4. Funding Process

- Investment Contributions: Investors commit funds to the loan. In many P2P platforms, the loan is funded in small increments by multiple investors, reducing the risk for any single investor.

- Loan Completion: Once the loan is fully funded, the platform disburses the loan amount to the borrower.

5. Repayment and Management

- Repayment Schedule: Borrowers make regular payments (typically monthly) to repay the loan. Payments include both principal and interest.

- Platform Administration: The P2P platform manages the loan servicing, including processing payments, handling collections, and distributing payments to investors.

6. Risk Management and Default Handling

- Risk Assessment: P2P platforms assess borrower risk and may offer different interest rates based on the risk profile. Some platforms also provide investors with risk mitigation tools, such as portfolio diversification.

- Default Handling: If a borrower defaults on the loan, the platform may attempt to recover the funds through collections or legal action. Investors may lose some or all of their investment if the borrower fails to repay.

7. Investor Returns

- Interest Income: Investors earn interest on their investment based on the loan’s terms and the borrower’s risk profile. Payments received from borrowers are distributed to investors proportionally based on their investment share.

- Returns Management: Investors can track their earnings and manage their investment portfolios through the platform’s dashboard.

Key Features of P2P Lending:

- Direct Transactions: Eliminates traditional banking intermediaries, allowing for direct transactions between borrowers and investors.

- Competitive Rates: Often offers competitive interest rates for both borrowers and investors, as the platform typically has lower overhead costs than traditional banks.

- Diversification: Investors can spread their investments across multiple loans to diversify risk.

- Alternative Data: Some platforms use alternative data sources to assess creditworthiness, potentially enabling borrowers with non-traditional credit histories to access loans.

Benefits and Considerations:

Benefits:

- For Borrowers: Easier access to loans, potentially lower interest rates, and a streamlined application process.

- For Investors: Opportunity to earn higher returns compared to traditional savings or investment products and the ability to diversify investment portfolios.

Considerations:

- Risk of Default: Investors face the risk of borrower default and may not recover their full investment.

- Platform Fees: P2P platforms typically charge fees for loan origination and servicing, which can impact returns.

- Regulatory Environment: The regulatory framework for P2P lending can vary, and platforms must comply with financial regulations and consumer protection laws.

Overall, P2P lending offers an alternative to traditional lending methods by leveraging technology to connect borrowers with investors, providing benefits for both parties while also introducing certain risks.

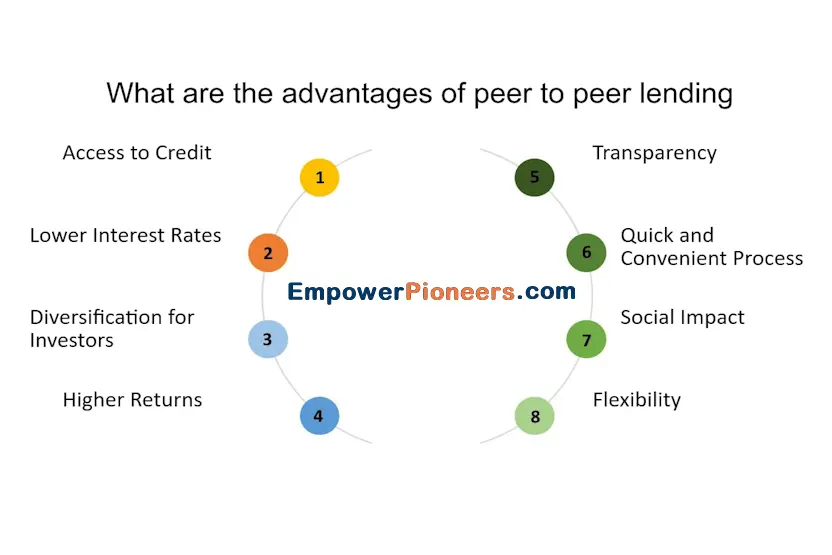

Peer-to-peer (P2P) lending offers several advantages for both consumers and businesses, making it an attractive alternative to traditional lending methods. Here’s a detailed look at the benefits for each:

Advantages for Consumers

- Access to Capital:

- Easier Approval: P2P lending platforms often have more flexible lending criteria compared to traditional banks, which can make it easier for individuals with lower credit scores or limited credit history to obtain a loan.

- Alternative Data: Some P2P platforms use alternative data (such as payment history and income) to assess creditworthiness, which can help borrowers who might not qualify through conventional means.

- Competitive Interest Rates:

- Lower Rates: Borrowers may benefit from lower interest rates due to the reduced overhead costs of P2P platforms compared to traditional banks. This is often achieved by removing intermediaries and leveraging technology for cost efficiency.

- Quick and Streamlined Process:

- Fast Approval and Funding: P2P platforms typically offer quicker loan approval and disbursement processes, allowing borrowers to access funds more rapidly than through traditional banks.

- Simplified Application: The application process is often straightforward and entirely online, reducing the time and paperwork required.

- Transparency:

- Clear Terms: P2P platforms usually provide transparent information about loan terms, fees, and interest rates, helping borrowers make informed decisions.

- Flexibility:

- Varied Loan Products: Borrowers can find a range of loan products to suit different needs, such as personal loans, debt consolidation, or medical expenses, often with customizable terms.

- Improved Financial Access:

- Financial Inclusion: P2P lending can offer access to credit for underserved or unbanked populations, including those who might be excluded from traditional financial services.

Advantages for Businesses

- Access to Funding:

- Alternative Financing: P2P lending provides an alternative to traditional bank loans, especially valuable for small and medium-sized businesses that may struggle to secure funding through conventional means.

- Diverse Funding Options: Businesses can access various types of loans, including working capital, equipment financing, and expansion funds, often tailored to their specific needs.

- Faster Funding:

- Quick Approval: The streamlined and efficient processes of P2P platforms can lead to faster loan approval and funding, which is critical for businesses needing immediate capital.

- Competitive Terms:

- Potential Cost Savings: P2P loans may offer competitive interest rates and favorable terms compared to traditional business loans, reducing the overall cost of borrowing.

- Flexible Loan Terms:

- Customizable Options: P2P platforms often provide flexible loan terms and repayment options, allowing businesses to negotiate terms that better fit their financial situation and cash flow.

- Increased Visibility:

- Showcase Business: By listing their loan needs on P2P platforms, businesses can gain exposure to a large pool of investors, potentially attracting attention and support from a broader audience.

- Reduced Bureaucracy:

- Streamlined Process: The application and approval process on P2P platforms is generally less bureaucratic and more streamlined than traditional banking processes, reducing administrative burden.

- Investor Interest:

- Access to a Broad Investor Base: P2P lending connects businesses with a wide range of investors, including individuals and institutions looking for investment opportunities, which can increase the likelihood of securing funding.

Overall Benefits:

- For Both Parties: P2P lending fosters a direct connection between borrowers and investors, often leading to better rates and terms for borrowers and attractive returns for investors.

- Innovation and Flexibility: The technology-driven approach of P2P lending platforms promotes innovation, flexibility, and efficiency, benefiting both consumers and businesses seeking funding solutions.

While P2P lending presents several advantages, borrowers and investors should also be aware of the associated risks, such as potential defaults and platform fees, and conduct thorough research before participating.

Peer-to-peer (P2P) lending platforms connect borrowers directly with individual or institutional investors, bypassing traditional financial intermediaries. These platforms offer both personal and commercial loans. Here’s a list of prominent P2P lending institutions in the U.S. specializing in personal loans and commercial loans for businesses:

Top 50 Peer-to-Peer Lending Institutions in the U.S.

Personal Loans:

- LendingClub

- Prosper

- Upstart

- Peerform

- Funding Circle (primarily business but offers personal loans as well)

- Social Finance (SoFi)

- Avant (not strictly P2P but offers similar personal loan products)

- Borrowell (U.S. presence)

- LendUp (focuses on personal loans with P2P elements)

- NetCredit (includes P2P features in its model)

- OneMain Financial (offers similar models)

- Best Egg (includes P2P-like options)

- Prosper Healthcare Lending (specializes in healthcare loans)

- Affirm (primarily point-of-sale financing)

- Upstart (also offers personal loans beyond its P2P roots)

- Earnest (includes elements of P2P)

- Clearbanc (primarily for business but includes personal loan options)

- Payoff (focuses on debt consolidation)

- Marble (offers personal loans with a P2P approach)

- SpringboardAuto (specializes in auto loans)

- FreedomPlus (offers P2P-like features)

- LightStream (primarily traditional but includes P2P-like elements)

- GoFundMe (not traditional P2P but includes loan elements)

- LendKey (offers P2P-like solutions for education loans)

- Enova (primarily alternative but includes P2P features)

Commercial Loans:

- Funding Circle

- StreetShares

- Kiva

- Lendio (connects borrowers with multiple P2P options)

- BlueVine (includes P2P-like business loans)

- OnDeck (includes P2P elements in its offerings)

- Fundation (primarily business but incorporates P2P models)

- Capify (includes P2P-like business financing)

- Credibly (includes P2P elements)

- National Funding (primarily traditional but includes P2P features)

- Rapid Finance (includes P2P elements)

- Dealstruck (primarily business with P2P-like features)

- Headway Capital (includes P2P business loan options)

- Finova Financial (includes P2P elements)

- Jitjatjo (specializes in business loans with P2P-like models)

- LendKey (includes P2P elements in business loans)

- Fundbox (includes P2P elements)

- Clearbanc (primarily business loans with P2P aspects)

- Harvest Small Business Finance (includes P2P-like models)

- StreetShares (includes P2P elements)

- Capitalize (includes P2P business loan models)

- LendingTree (connects to P2P options)

- Upstart Business (includes P2P aspects)

- Kiva (specializes in microloans)

- Business Backer (includes P2P-like models)

Notes:

- Personal Loans: P2P platforms provide direct lending opportunities for personal needs such as debt consolidation, home improvement, and other expenses.

- Commercial Loans: P2P platforms cater to businesses seeking funding for various purposes, including expansion, working capital, and equipment purchases.

These platforms offer a range of features and loan products, so it’s important to evaluate each based on your specific financial needs and preferences.

--- article sharing ---