July 4th, 2026

Generally, Fintech companies, short for “financial technology” companies, use technology to improve and automate financial services and processes.

These companies are transforming the financial industry by offering innovative solutions and services that make financial transactions and management more efficient, accessible, and user-friendly.

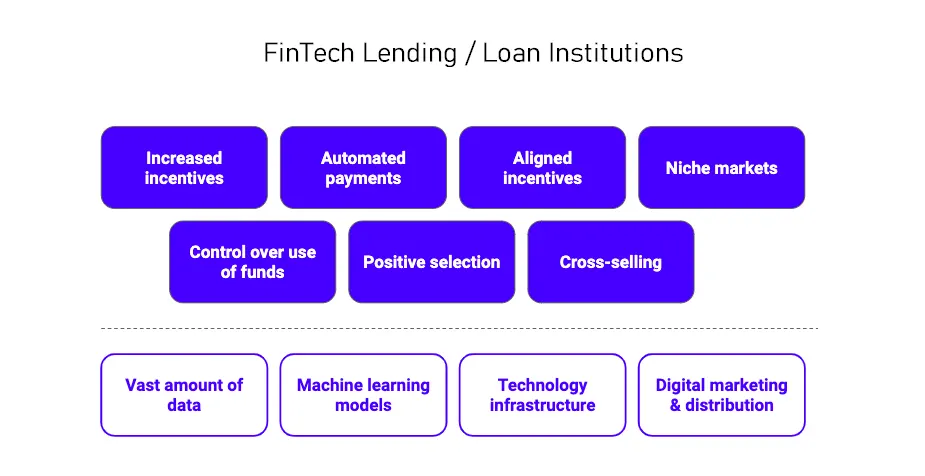

Fintech companies specializing in personal and commercial loans have significantly impacted the lending industry in several ways.

Their innovations have brought both opportunities and challenges to borrowers and traditional lenders alike.

In the past decade, advancements in financial technology have highlighted a new wave of lenders in the personal loan market — Fintech lenders.

While traditional institutions like banks, credit unions, and finance companies remain crucial in offering personal loans, Fintech lenders have significantly increased their market presence.

This article offers an overview of the Fintech sector, drawing insights from two relatively recent data sources.

Here’s a breakdown of the key impacts:

1. Increased Accessibility and Inclusivity

- Broader Reach: Fintech lenders often use digital platforms to reach underserved or unbanked populations who might not have access to traditional banking services.

- Simplified Processes: Online applications and automated approval processes make it easier for individuals and businesses to apply for and receive loans without needing to visit a physical branch.

2. Faster and More Efficient Processes

- Quick Approvals: Many fintech lenders use algorithms and data analytics to evaluate creditworthiness, which can lead to faster loan approvals and disbursements compared to traditional banks.

- Streamlined Applications: The application process is often simplified, requiring less paperwork and reducing the time needed to secure a loan.

3. Enhanced Customer Experience

- User-Friendly Platforms: Fintech companies offer intuitive digital interfaces, allowing borrowers to manage their loans, make payments, and track their loan status easily through mobile apps or websites.

- Personalized Services: Advanced data analytics enable fintech lenders to offer personalized loan products and terms based on the borrower’s financial profile and needs.

4. Increased Competition and Innovation

- Pressure on Traditional Lenders: The rise of fintech lenders has introduced competition to traditional banks, prompting them to innovate and improve their own loan offerings.

- New Loan Products: Fintech companies often introduce novel loan products and flexible terms that cater to specific borrower needs, such as short-term loans, microloans, or tailored financing options for niche markets.

5. Data-Driven Decision Making

- Enhanced Risk Assessment: Fintech lenders use alternative data sources, such as social media activity, transaction history, and other non-traditional data points, to assess creditworthiness and mitigate risk.

- Predictive Analytics: Advanced analytics help in predicting borrower behavior and improving loan underwriting processes, leading to more informed lending decisions.

6. Cost Efficiency and Lower Interest Rates

- Reduced Overheads: Digital-first models often result in lower operational costs for fintech lenders, which can translate into lower interest rates and fees for borrowers.

- Transparent Pricing: Many fintech companies offer transparent fee structures and competitive rates, enhancing affordability and cost-effectiveness for borrowers.

7. Greater Flexibility and Customization

- Tailored Loan Products: Fintech lenders often provide more flexible loan options, including varying repayment terms and customized loan amounts, to meet the specific needs of individuals and businesses.

- Innovative Repayment Options: Some fintech companies offer flexible repayment schedules and automatic payment options to accommodate borrowers’ financial situations.

8. Financial Education and Resources

- Educational Tools: Many fintech lenders provide educational resources and tools to help borrowers understand loan terms, manage debt, and make informed financial decisions.

- Financial Health Monitoring: Some platforms offer features to monitor and improve credit scores, providing additional value to borrowers beyond just lending.

9. Impact on Traditional Credit Scoring

- Alternative Credit Scoring: By incorporating alternative data into credit assessments, fintech companies challenge traditional credit scoring models and provide opportunities for those with limited credit histories to secure loans.

- Enhanced Credit Access: This can lead to broader credit access for individuals and businesses who may not have been able to secure loans through conventional means.

10. Regulatory and Security Challenges

- Regulatory Adaptation: The rapid growth of fintech lending has led to increased regulatory scrutiny, as traditional regulations may not fully cover new fintech practices. Companies must navigate evolving regulatory landscapes.

- Data Security: As fintech companies handle sensitive financial data, ensuring robust cybersecurity measures is crucial to protect against breaches and fraud.

11. Potential Risks and Drawbacks

- Over-Lending Risk: The ease of accessing credit through fintech platforms may lead to over-lending or over-borrowing, potentially resulting in financial strain for borrowers.

- Variable Quality of Service: The quality of service and borrower experience can vary significantly among fintech lenders, so borrowers need to carefully review and compare options.

Overall, fintech companies specializing in personal and commercial loans have introduced significant positive changes to the lending landscape, making borrowing more accessible, efficient, and tailored. However, they also present challenges and risks that borrowers and regulators must navigate carefully.

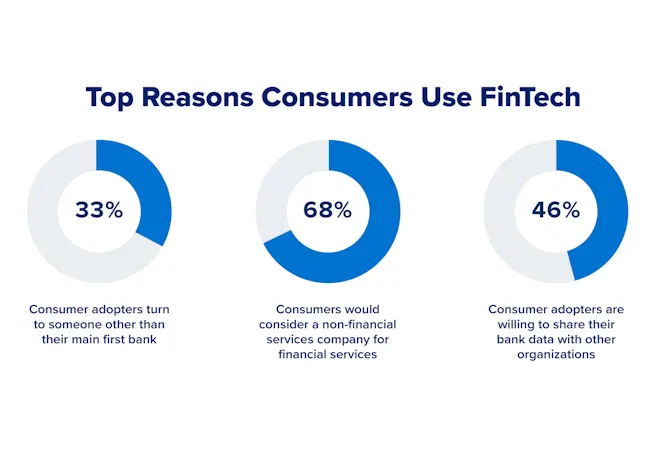

consumer adoption rates are impressive (210 million Americans use Fintech products), the investments and deals being made on Wall Street are even more eye-popping. In 2015 there were 1,994 Fintech investments made (globally) worth $21.8 billion. By 2021, however, that number climbed to 3,549 deals worth $94.1 billion (a 327% growth rate over six years).

Here’s a broad overview of what fintech companies do and how they impact the financial landscape:

Types of Fintech Companies

Function: Allow individuals or businesses to raise funds for projects or ventures through contributions from a large number of people.

Digital Payments and Transfers

Examples: PayPal, Square, Venmo, Stripe

Function: Facilitate electronic payments and money transfers, often with lower fees and greater convenience compared to traditional banking methods.

Online Banking and Neobanks

Examples: Chime, N26, Revolut

Function: Offer banking services entirely online, including checking and savings accounts, without physical branches.

Lending Platforms

Examples: LendingClub, SoFi, Prosper

Function: Provide personal loans, peer-to-peer lending, or business loans through online platforms, often with more flexible terms and quicker approvals compared to traditional banks.

Investment and Wealth Management

Examples: Robinhood, Betterment, Wealthfront

Function: Offer tools and platforms for investing and managing wealth, often with lower fees and automated investment options.

Insurance Technology (Insurtech)

Examples: Lemonade, Metromile, Root Insurance

Function: Use technology to provide innovative insurance products, streamline the underwriting process, and improve claims management.

Robo-Advisors

Examples: Betterment, Acorns, Stash

Function: Use algorithms and automated systems to provide investment advice and portfolio management services at lower costs.

Regtech (Regulatory Technology)

Examples: ComplyAdvantage, Trulioo

Function: Offer solutions for regulatory compliance, fraud detection, and risk management, helping companies adhere to financial regulations more efficiently.

Blockchain and Cryptocurrencies

Examples: Coinbase, Binance, Ripple

Function: Use blockchain technology to offer digital currencies, smart contracts, and decentralized financial systems.

Personal Finance and Budgeting

Examples: Mint, YNAB (You Need A Budget), Personal Capital

Function: Provide tools for budgeting, expense tracking, and financial planning to help individuals manage their finances more effectively.

Crowdfunding Platforms

Examples: Kickstarter, Indiegogo, GoFundMe

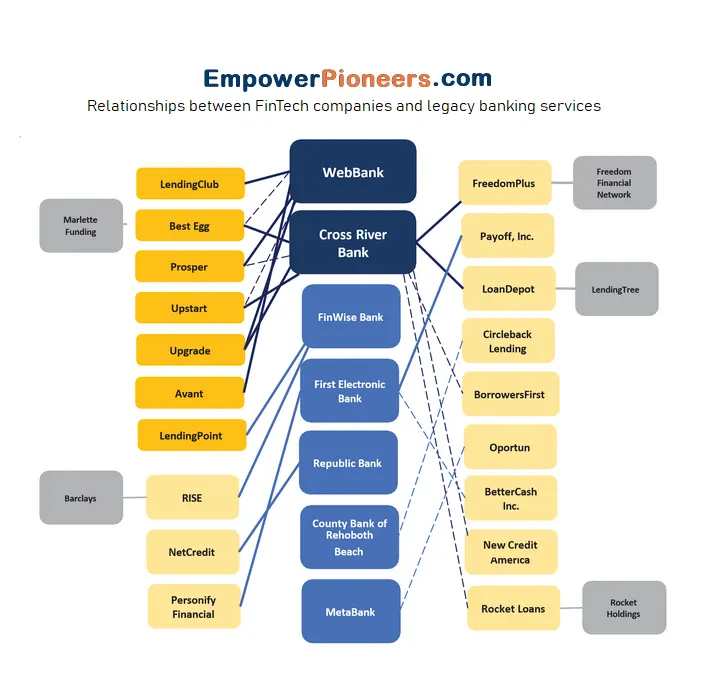

Banks are increasingly viewing these alternative lenders as potential partners rather than disrupters. Banks are associating with Fintech lenders in a number of ways. They range from providing origination services and funding to customer referrals. In some cases, these associations are seamless to customers so that the relationship with the bank is maintained. For examples, Fintech firms such as the Lending Club and Prosper are turning to commercial banks and industrial banks to originate their loans.

Banks are also making equity investments in Fintech firms avoiding the cost of in-house development:

Fifth Third’s investment in ApplePie Capital (online lender specializing in franchise loans) is one example.

Bank Alliance, a network of over 200 banks, partners with the Lending Club and Fundation to allow members to offer small dollar consumer and business loans.

Members may also purchase loans from these Fintech firms to add to their balance sheets. In addition, JPMorgan Chase has licensed technology from OnDeck to offer Chase customers small business loans in an entirely digital process.

The loans are Chase-branded and held on the bank’s balance sheet, where JPMorgan sets the underwriting criteria for the loans.

Overall Impact of Fintech Companies

- Increased Accessibility

- Financial Inclusion: Fintech solutions make financial services more accessible to underserved or unbanked populations, often through mobile devices and online platforms.

- Enhanced Convenience

- User Experience: Fintech companies streamline financial processes, making tasks like transferring money, applying for loans, and investing more convenient and user-friendly.

- Cost Savings

- Lower Fees: Many fintech solutions reduce or eliminate traditional banking fees and offer more competitive rates for financial services.

- Innovation and Competition

- Market Disruption: By introducing new technologies and business models, fintech companies challenge traditional financial institutions, leading to greater innovation and improved services across the industry.

- Data-Driven Insights

- Personalization: Fintech companies often use data analytics to provide personalized financial advice and services, enhancing the overall customer experience.

- Security and Transparency

- Advanced Technology: Many fintech companies use advanced security measures, such as encryption and biometric authentication, to protect user data and transactions.

In credit bureau data, Fintech lender balances are distributed across various sectors. Finance companies account for the largest portion of Fintech-issued loans, with $32.2 billion, making up 39% of their total personal loan balances.

Within this sector, personal loan companies and miscellaneous companies hold similar amounts of Fintech-issued balances—$15.5 billion and $16.7 billion, respectively—though these amounts represent different proportions of their overall holdings: 29% for personal loan companies and 79% for miscellaneous companies.

Sales finance companies have a minimal share of Fintech loans. Among depository institutions, banks are the primary holders of Fintech-issued loans, with $17.7 billion, which constitutes 10% of their total personal loans and 6.5% of the total personal loan holdings within depository institutions.

In terms of outstanding loans and balances, the Fintech sector is significantly larger than the finance company sector, with nearly $50 billion in balances and 7.6 million accounts, compared to $18 billion and 4.2 million accounts for finance companies.

However, the Fintech sector is smaller than the depository institutions sector, which holds $74.5 billion in balances and 9 million accounts.

The median account balance for Fintech loans is $4,371, which is similar to the $4,154 median balance for depository institutions and notably higher than the $2,613 median balance for finance companies.

Fintech-issued loans generally have maturities comparable to those from banks but are longer than those from finance companies, with average maturities of 2.3 years, 2.5 years, and 1.4 years, respectively.

The median monthly payment for a Fintech loan is $200, which is $36 higher than the payment on a finance company loan but $10 lower than that on a personal loan from a depository institution.

For consumers, Fintech companies attempt to offer easier, more convenient, and more streamlined financial services. Most of which are designed to grab market share from traditional financial services companies and the legacy banking system.

For businesses, Fintech companies aim to help clients reduce expenses while improving the speed and efficiency of their systems, processes and operations.

Overall, fintech companies are reshaping the financial landscape by leveraging technology to offer more efficient, accessible, and personalized financial services.

Here’s a list of prominent fintech lending institutions in the U.S. that specialize in both personal loans and commercial loans for businesses. This list includes a mix of well-known players and innovative startups in the fintech space:

Top 50 Fintech Lending Institutions in the U.S.

Personal Loans:

- SoFi

- LendingClub

- Prosper

- Upstart

- Avant

- Marble

- Best Egg

- Earnest

- Affirm

- Upgrade

- Payoff

- Peerform

- NetCredit

- Clearbanc

- LightStream

- OneMain Financial

- Cabbage

- SpringboardAuto

- Tally

- FreedomPlus

- GoFundMe

- LoanClub

- LendKey

- Enova

- Prosper Healthcare Lending

Commercial Loans:

- Kabbage

- Fundbox

- BlueVine

- OnDeck

- Credibly

- Square Capital

- Funding Circle

- PayPal Working Capital

- LoanBuilder (a PayPal service)

- Business Backer

- Rapid Finance

- Dealstruck

- National Funding

- StreetShares

- Jitjatjo

- Headway Capital

- Capify

- SBA 7(a) Loans via online platforms

- Fundation

- Harvest Small Business Finance

- Finova Financial

- Lendio

- Braintree (a PayPal service)

- Upstart Business

- IFunding