July 29th, 2026

Using a home equity loan or a Home Equity Line of Credit (HELOC) can be a strategic way to finance major expenses such as home improvements, education costs, or debt consolidation.

Both options allow you to borrow against the equity in your home, often at lower interest rates compared to personal loans or credit cards.

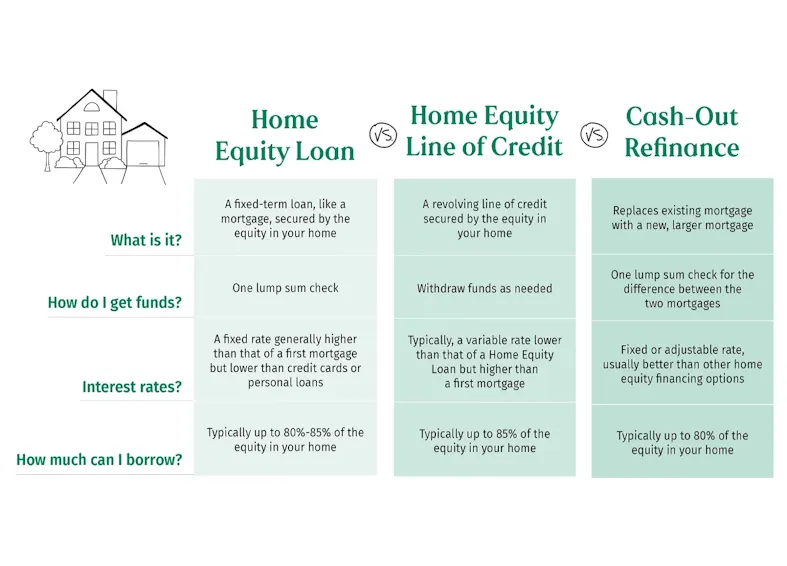

A home equity loan provides a lump sum with fixed interest rates and repayment terms, making it suitable for one-time expenses like a major renovation.

On the other hand, a HELOC offers a revolving line of credit with variable interest rates, giving you the flexibility to draw funds as needed, which is ideal for ongoing expenses or projects.

It’s important to use these funds wisely and ensure you have a solid repayment plan, as your home serves as collateral.

Home Equity Loan or a Home Equity Line of Credit (HELOC)

Using a Home Equity Loan or a Home Equity Line of Credit (HELOC) can be a strategic way to finance major expenses, but it’s important to approach it with a clear understanding of how these options work and what they entail.

Using a Home Equity Loan or a Home Equity Line of Credit (HELOC) can be an effective way to cover significant expenses, leveraging the value of your home to access funds.

A Home Equity Loan provides a lump sum of money with a fixed interest rate and term, making it suitable for one-time, large expenses.

For instance, if you’re planning a major home renovation, such as a kitchen remodel that costs $30,000, a Home Equity Loan allows you to borrow the full amount upfront.

You’ll then repay this amount over a set period—typically 5 to 15 years—through fixed monthly payments.

This predictability helps in budgeting since the loan terms and payments remain constant throughout the life of the loan.

Here’s a guide on how to use them effectively:

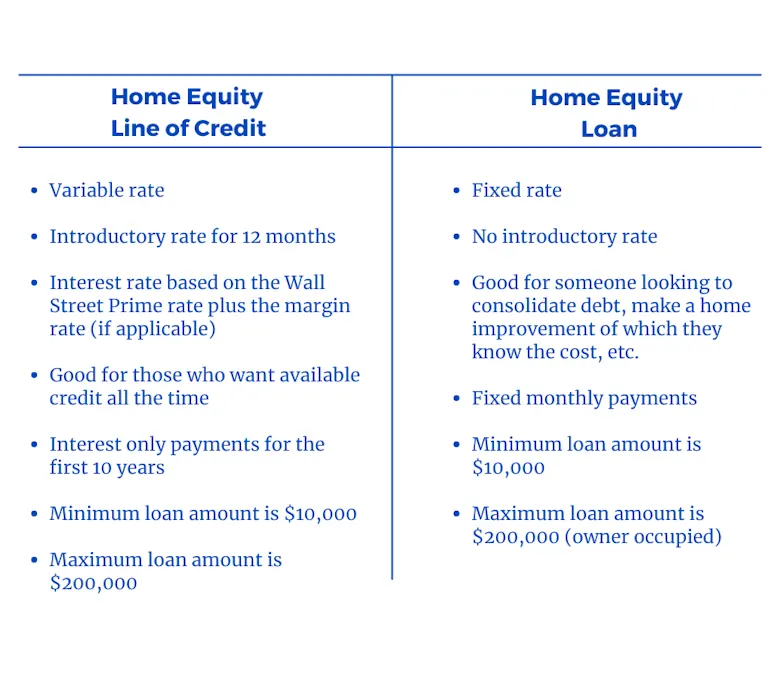

Home Equity Loan vs. HELOC

- Home Equity Loan:

- Definition: A lump-sum loan with a fixed interest rate and fixed repayment term.

- Best For: Large, one-time expenses (e.g., home renovations, debt consolidation).

- Repayment: Fixed monthly payments over a set period.

- HELOC:

- Definition: A revolving line of credit with a variable interest rate.

- Best For: Ongoing or flexible expenses (e.g., education costs, ongoing home improvement).

- Repayment: You borrow as needed during the draw period and make monthly payments based on the balance.

Steps to Use a Home Equity Loan or HELOC

- Assess Your Financial Situation:

- Determine Your Equity: Calculate your home equity by subtracting your mortgage balance from your home’s current market value. Lenders typically allow you to borrow up to 80-90% of your home equity.

- Check Your Credit Score: A higher credit score can secure better interest rates.

- Evaluate Your Budget: Ensure you can handle the new monthly payments alongside your existing financial obligations.

- Research Lenders:

- Compare Rates and Terms: Look for competitive interest rates, fees, and loan terms. Consider both traditional banks and credit unions.

- Read Reviews: Check lender reviews and customer satisfaction scores to gauge reliability and service quality.

- Apply for the Loan or HELOC:

- Gather Documentation: Typically, you’ll need income verification, tax returns, and information about your home.

- Submit an Application: Complete the application process, which may involve an appraisal of your home and a review of your financial history.

- Use the Funds Wisely:

- Home Equity Loan: Use the lump sum for planned expenses where you need a fixed amount of money. For instance, if you’re doing a major home renovation, a home equity loan can provide the full amount upfront.

- HELOC: Use the line of credit for flexible or ongoing expenses. Draw funds as needed, and be mindful of the variable interest rates that can change over time.

- Manage Repayments:

- Home Equity Loan: Stick to the fixed monthly payments and budget for the term of the loan.

- HELOC: Monitor your spending and repayments. Pay off the balance during the draw period if possible to reduce the total interest paid.

- Plan for Interest Rate Changes:

- Home Equity Loan: Fixed rates mean your payments won’t change.

- HELOC: Variable rates can fluctuate, so be prepared for potential increases in your monthly payments.

- Consider the Risks:

- Home Equity Loan: If you default, you risk foreclosure since your home is collateral.

- HELOC: Variable rates and borrowing costs can increase, and if your financial situation changes, it might be harder to repay.

Tips for Success

- Budget Carefully: Ensure that the new loan payments fit comfortably within your budget.

- Keep Track of Your Home’s Value: If your home’s value decreases, it could affect your ability to access future credit.

- Consult a Financial Advisor: Before making significant financial decisions, getting advice from a financial advisor can provide personalized guidance.

HELOC functions more like a credit card with a revolving balance and variable interest rates.

It provides flexibility to draw funds as needed up to a certain limit, making it ideal for ongoing or fluctuating expenses.

For example, if you’re funding your child’s education or managing multiple home improvement projects, a HELOC allows you to borrow and repay as necessary.

During the draw period, you only pay interest on the amount borrowed, which can be beneficial if you need to access funds intermittently.

However, the variable interest rate means your payments can fluctuate, so it’s crucial to plan for potential rate increases.

Using home equity wisely can provide the necessary funds for major expenses, but it requires careful planning and management to ensure it benefits your financial situation in the long run.

Equity debt financing options come with significant risks, primarily because your home serves as collateral.

For a Home Equity Loan, missing payments can lead to foreclosure, as the lender has a claim on your property.

With a HELOC, while the variable rates can affect your payment amounts, the revolving nature of the credit line means you must carefully manage your withdrawals and repayments.

It’s essential to evaluate your financial stability and ensure you can handle the additional debt before proceeding with either option.

Consulting with a financial advisor can provide tailored advice to navigate these choices effectively and align them with your financial goals.

Insider industry experts offer valuable insights on Home Equity Loan or HELOC

Insider industry experts offer several valuable insights on effectively using a Home Equity Loan or HELOC for major expenses. Here are some key strategies and secrets to maximize these financial tools:

1. Optimize Timing and Interest Rates

Secret: Timing can significantly impact the cost-effectiveness of a Home Equity Loan or HELOC. Industry experts recommend taking advantage of favorable market conditions to secure the best interest rates. For instance, if interest rates are low, locking in a Home Equity Loan can lead to substantial savings over the life of the loan. Conversely, for a HELOC, it’s beneficial to open the line of credit during a period of low variable rates. Additionally, some experts suggest monitoring economic indicators and market trends to choose an optimal time for borrowing, especially if you expect rates to rise.

Example: If the Federal Reserve is signaling an interest rate hike, securing a Home Equity Loan now could save you from paying higher rates in the future. For a HELOC, consider drawing funds before anticipated rate increases to lock in lower borrowing costs during the draw period.

2. Leverage Loan Features to Your Advantage

Secret: Both Home Equity Loans and HELOCs come with features that can be strategically used to manage expenses. With a Home Equity Loan, experts advise taking advantage of the fixed interest rate to budget effectively. However, if you anticipate needing flexibility, a HELOC allows you to borrow only what you need and repay it on a flexible schedule. Some HELOCs offer promotional periods with lower rates or fee waivers, so leveraging these introductory offers can save money.

Example: If you’re undertaking a major renovation with variable costs, a HELOC’s flexibility allows you to draw funds as needed rather than borrowing a lump sum. Utilize any promotional offers for reduced fees or introductory rates to minimize initial costs. Once the project is complete, you can focus on paying down the balance.

3. Monitor and Manage Risk Strategically

Secret: Managing risk is crucial when using home equity products. Experts recommend setting up automatic payments to avoid missing deadlines, which can lead to foreclosure. Additionally, regularly review your financial situation and adjust your repayment strategy as needed. For HELOCs, experts suggest maintaining a budget that accounts for potential rate increases. Some lenders offer options to convert a portion of your HELOC balance to a fixed-rate loan, providing stability in uncertain interest rate environments.

Example: If your HELOC balance becomes substantial and interest rates rise, consider converting part of the balance to a fixed-rate portion to lock in stable payments. This strategy helps mitigate the impact of rate volatility on your overall debt repayment.

By understanding and applying these insider secrets, you can more effectively use Home Equity Loans and HELOCs to manage major expenses, ensuring that you leverage these financial tools in a way that aligns with your long-term financial goals.

The Best Lenders for Home Equity Loans or HELOCs

When looking for the best lenders for Home Equity Loans or HELOCs, especially if you have less-than-perfect credit, it’s essential to consider a combination of factors: flexibility, competitive rates, low fees, and a streamlined application process. Here are some top lenders known for their favorable terms and accessible services:

1. Discover Home Equity Loans

Why They’re Great:

- Flexibility: Discover offers both Home Equity Loans and HELOCs with flexible terms and no annual fees.

- Rates and Fees: They provide competitive fixed rates for Home Equity Loans and variable rates for HELOCs. Discover is known for its transparency and low fees, including no origination fees.

- Application Process: Their online application process is straightforward and quick, with a strong reputation for customer service.

- Approval Rates: Discover considers a range of credit scores and offers prequalification options, which can be useful if your credit isn’t perfect.

Example: If you need a Home Equity Loan for a specific project and have a decent credit score, Discover’s fixed rates and no-fee structure can be particularly advantageous.

2. Home Depot Credit Card (Home Improvement Projects)

Why They’re Great:

- Flexibility: Although not a traditional HELOC or Home Equity Loan, the Home Depot Credit Card offers promotional financing options that can be used for home improvement projects.

- Rates and Fees: They offer special financing options with deferred interest promotions. However, it’s crucial to understand the terms and conditions to avoid high-interest rates if the balance is not paid off within the promotional period.

- Application Process: The application process is relatively simple, and approval can be more lenient compared to traditional lenders.

- Approval Rates: Home Depot Credit Card often has more flexible credit requirements, making it accessible for those with less-than-perfect credit.

Example: For smaller home improvement projects, the Home Depot Credit Card can offer a convenient way to manage expenses with promotional financing.

3. Credit Unions (e.g., Navy Federal Credit Union, PenFed Credit Union)

Why They’re Great:

- Flexibility: Credit unions are known for offering flexible terms and personalized service. They often provide both Home Equity Loans and HELOCs.

- Rates and Fees: They typically offer lower interest rates and fewer fees compared to traditional banks. Some credit unions may have membership requirements but often provide competitive rates and terms.

- Application Process: Credit unions generally have a reputation for a more personalized application process, which can be advantageous if you have less-than-perfect credit.

- Approval Rates: Credit unions may be more lenient with credit score requirements and focus on overall financial health rather than just credit scores.

Example: If you are a member of a credit union like Navy Federal or PenFed, you might benefit from lower rates and more flexible terms, even with a lower credit score.

4. SoFi

Why They’re Great:

- Flexibility: SoFi offers Home Equity Lines of Credit with flexible borrowing options and competitive rates.

- Rates and Fees: Known for their competitive rates and no fees for account setup, SoFi focuses on providing transparency.

- Application Process: The application process is streamlined and entirely online, making it convenient and quick.

- Approval Rates: SoFi considers various factors beyond just credit scores, including overall financial health and potential.

Example: SoFi can be an excellent choice for those who want an entirely digital process with competitive rates and a focus on holistic financial evaluation.

5. USAA

- Flexibility: Specializes in HELOCs with flexible terms and a fast application process.

- Rates and Fees: Competitive rates and low fees; some fees may be waived for military members.

- Application Processing: Simple online application process.

- Approval Rates: Considerate of military members’ financial situations, including those with less-than-perfect credit.

6. Figure

- Flexibility: Provides Home Equity Loans and HELOCs with a range of term options.

- Rates and Fees: Competitive rates with no hidden fees. They offer a fully online process with transparency in terms and costs.

- Application Processing: Efficient online application process with various tools for understanding loan options.

- Approval Rates: Known for being more lenient with credit scores due to their advanced technology and data-driven approach.

7. Wells Fargo

- Flexibility: Offers both Home Equity Loans and HELOCs with adjustable terms.

- Rates and Fees: Competitive rates with relatively low fees.

- Application Processing: User-friendly online application with helpful tools and resources.

- Approval Rates: Provides options for borrowers with less-than-perfect credit.

8. Chase

- Flexibility: Provides Home Equity Loans and HELOCs with flexible terms.

- Rates and Fees: Competitive rates and various fee structures.

- Application Processing: Easy online application with strong customer support.

- Approval Rates: Generally considers a broad range of credit scores.

9. LendingTree

- Flexibility: Acts as a marketplace to compare offers from various lenders, including Home Equity Loans and HELOCs.

- Rates and Fees: Provides access to multiple lenders with competitive rates and fees.

- Application Processing: Streamlined process for comparing offers from different lenders.

- Approval Rates: By comparing multiple lenders, you can find options even with less-than-perfect credit.

10. Quicken Loans (Rocket Mortgage)

- Flexibility: Provides a range of home equity products with flexible terms.

- Rates and Fees: Competitive rates with a clear fee structure.

- Application Processing: Fully online application process with robust support and technology.

- Approval Rates: Uses advanced technology to assess a broad range of credit profiles.

11. Purdue Federal Credit Union

Why They’re Great:

- Flexibility: Offers both Home Equity Loans and HELOCs with a range of term options.

- Rates and Fees: Known for competitive rates and lower fees compared to traditional banks. They often provide special offers for credit union members.

- Application Processing: Straightforward online application process with personalized service.

- Approval Rates: More flexible with credit requirements, focusing on overall financial health.

Example: As a smaller credit union, Purdue Federal can offer competitive terms and flexibility that might be beneficial for borrowers with less-than-perfect credit.

12. Alliant Credit Union

Why They’re Great:

- Flexibility: Provides both Home Equity Loans and HELOCs with flexible borrowing options.

- Rates and Fees: Offers competitive rates and low fees, often with special promotions for credit union members.

- Application Processing: User-friendly online application with quick processing times.

- Approval Rates: More accommodating to borrowers with varying credit profiles.

Example: Alliant Credit Union’s combination of competitive rates and flexible terms makes it a strong option for those seeking a more personalized lending experience.

13. OneMain Financial

Why They’re Great:

- Flexibility: Specializes in personal loans but also offers Home Equity Loans with flexible terms.

- Rates and Fees: Known for working with borrowers who have less-than-perfect credit, with competitive rates and clear fee structures.

- Application Processing: Easy application process with quick decisions and funds available relatively fast.

- Approval Rates: Has a reputation for accommodating a wide range of credit scores.

Example: For those needing a Home Equity Loan and facing credit challenges, OneMain Financial’s willingness to work with various credit profiles can provide a viable option.

14. Apex Bank

Why They’re Great:

- Flexibility: Offers Home Equity Loans and HELOCs with customizable terms.

- Rates and Fees: Provides competitive rates and low fees, with a focus on customer service.

- Application Processing: Simplified application process with personalized attention.

- Approval Rates: More flexible with credit requirements, particularly for local customers.

Example: Apex Bank’s local focus and personalized service make it a good choice for those looking for more tailored lending solutions.

15. RCU (Redwood Credit Union)

Why They’re Great:

- Flexibility: Provides a range of Home Equity products with flexible terms.

- Rates and Fees: Competitive rates and low fees, with a focus on member satisfaction.

- Application Processing: Efficient online application process with strong customer service.

- Approval Rates: More accommodating to members with less-than-perfect credit.

Example: Redwood Credit Union’s commitment to member service and competitive rates makes it an attractive option for those needing flexible home equity financing.

16. LendingPoint

Why They’re Great:

- Flexibility: Specializes in personal loans but also offers Home Equity products with flexible terms.

- Rates and Fees: Provides competitive rates and clear, upfront fee structures.

- Application Processing: Fast and straightforward online application process.

- Approval Rates: Known for working with borrowers with various credit profiles.

Example: LendingPoint’s flexibility and quick processing can be advantageous for those seeking home equity financing with less-than-perfect credit.

17. Upgrade

Why They’re Great:

- Flexibility: Offers HELOCs and personal loans with flexible terms.

- Rates and Fees: Competitive rates with low fees and transparent pricing.

- Application Processing: Easy online application process with quick approvals.

- Approval Rates: More flexible with credit profiles, focusing on overall financial health.

Example: Upgrade’s user-friendly platform and competitive terms make it a good choice for those needing flexible home equity financing.

18. Horizon Credit Union

Why They’re Great:

- Flexibility: Provides Home Equity Loans and HELOCs with a range of term options.

- Rates and Fees: Competitive rates and lower fees compared to traditional banks.

- Application Processing: Simplified online application with responsive customer service.

- Approval Rates: More lenient with credit scores, focusing on member relationships.

Example: Horizon Credit Union’s local approach and flexible terms can benefit those with less-than-perfect credit seeking home equity options.

Tips for Selecting a Lender:

- Compare Offers: Use comparison tools or speak with a financial advisor to evaluate offers from multiple lenders.

- Check Fees: Be mindful of any fees that may apply, including application fees, appraisal fees, or early repayment penalties.

- Understand Terms: Ensure you understand the terms of the loan or line of credit, including interest rates, repayment schedules, and any potential rate adjustments.

When exploring these options, it’s beneficial to contact each lender directly to discuss your specific needs and financial situation, ensuring you get the best possible terms and rates based on your credit profile and financial goals.

By carefully evaluating these lenders and their offers, you can find a Home Equity Loan or HELOC that best meets your needs, whether you’re looking for flexible terms, great rates, or a streamlined application process.

--- article sharing ---