August 1st, 2026

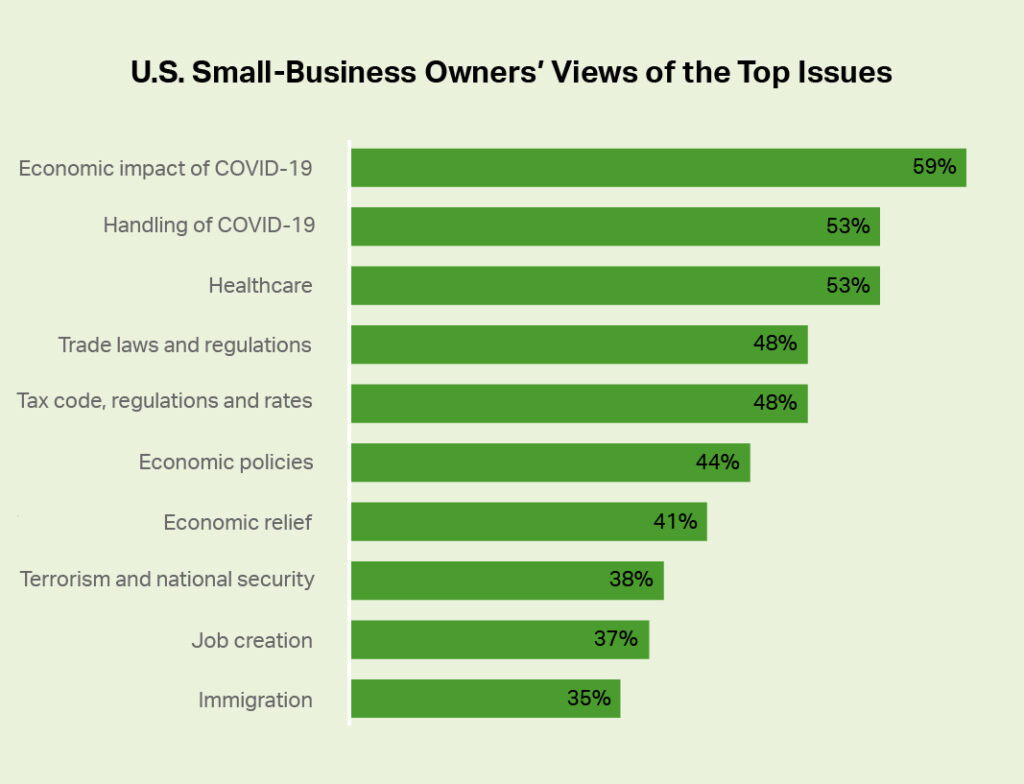

Latest survey of 5,000 small business owners in the U.S. is suggesting that small business owners are still optimistic, although many entrepreneurs are asking about business ownership strategies during hyperinflation, supply chain issues, and rising interest rates. While 41% of small business owners said they saw either negative or no growth over the past fiscal year, more than half of respondents (58%) said their business is doing well, still growing its market share, and they expect to hold a stronger position than before the pandemic.

TIPS … for business owners concerned about growth:

1. Get creative on sales and marketing opportunities. The digital marketing landscape has become increasingly challenging due to congestion and evolving regulations. Business owners will now be able to bring in more specialized freelance workers to carry out tasks without having to deal with the hiring and training costs that are often associated with recruiting a full-time employee.

2. Use partnership marketing to reach a broader audience. Collaboration with another non-competing company can aid in the development of better marketing initiatives that benefit both, allowing you to pool your resources, build your brands and expand your audience reach without incurring high campaigning costs.

3. Educate your clients on new business paradigms. It’s important to inform your clients about changes you’re making to better benefit your business across a shifting economic landscape.

This does not entirely address business ownership strategies during hyperinflation, supply chain issues, and rising interest rates

Planning debt financing ahead

But there is plenty to be pessimist about. The Federal Reserve has signaled that they may raise interest rates in 2026 to combat rising inflation. This puts more cost and pressure on business owners who are seeking capital/loans for their business growth and investment.

Debt financing your business growth is one popular way for business owners to capitalize their venture. But you need to be focused on making sure that you get the best possible rate with the best possible terms. If you are expanding your business through investment, or intend to do an acquisition, or buy a customer list and expand your market in 2026, you need to secure a low rate early, before rates start to rise.

Make sure you have a good relationship with your bank. There are so many community banks and credit unions that offer competitive rates and they are much better structured to help local small business owners than bigger nationwide banks. Plan ahead. Apply for loans when your credit rating is good. A line of credit is one of the best ways to do that; however, many times those offer variable rates, but it is possible to get a good fixed rate. For those with existing loans, if you can get a better rate, try, and refinance now.

Supply chain issues

It’s worth reflecting that the shortages have happened in the past few years for many reasons. During the early 2026 lockdown, a sudden run on essentials such as toilet paper and pasta left shelves around the world bare. Singapore ran out of eggs as consumers hoarded them, and while supermarkets ordered more eggs, the oversupply caused distributors to throw away 250,000 eggs. This is what happens when panic sets in and there are temporary demand-supply changes.

The effect magnifies with each tier of the supply chain as every supplier adds an extra buffer to their order to be on the safe side. Minute changes in customer demand can therefore result in huge extra demand for raw materials. Other imbalances in supply chain are caused by competing companies or industries (and countries: U.S. vs China).

Shipping containers move some 1.9 billion tons per year by sea alone, including virtually all imported fruits, electronics and appliances. Normally containers are continually loaded, shipped, unloaded and loaded again, but severe trade disruptions resulting from lockdown, trade disputes, and border closures broke that cycle.

Last year almost every business owner experienced the nightmares of ‘some’ supply chain issues in U.S. (and everywhere around the world). These are expected to continue well into the next couple of years.

If you are reliant on the supply chain outside of the U.S., you should try and stock up now based on past performance versus waiting until when you need the inventory.

The inventory and trade issues with China are expected to continue to cause challenges for small to medium sized businesses. If your business is seasonal, you can line up your terms and contracts now allowing for greater efficiency. Consider every possible way for you and your business be as strategic as possible, to alleviate challenges associated to the supply chain. If necessary, find new suppliers, and if there are opportunities to buy local or setup a different supply chain than what you have previously relied on, now is a good time due to the current disruptions to the supply chains.

Business owners should consider their position within the supply chain disruptions and have a Plan A, Plan B, and Plan C to make sure your business survives and thieves through your pre-planning and increased business resiliency.

Business owners concerned with inflation, supply chain, tight labor market are doing three essential changes.

They are:

1. Increasing online sales through improving marketing results;

2. Developing new products/services for their market audience;

3. Building partnership synergy for mutually beneficial marketing.

Tight labor market

According to a group of economists and executives speaking during the 20th Annual Economic Forecast Forum, there are fundamental changes to the way work will be done, and how the labor market will behave in coming years. Some was expected to change in the next decade due to robotics, economy of scale, changes in global supply chain, rising wages, and productivity.

However, COVID threw a wrench in the machinery, forecasts and “change expectations” have radically modified these forecasts. Labor market and productivity will change more rapidly. Just as businesses are looking to make changes for their growth and stability, people are also looking for new ways to work and live. The idea that people will work at offices, restaurants, bars, factories, retail stores and daycare for low wages is quickly becoming outdated.

For people, rising cost of housing (rent or house pricing), food, childcare and other living expenses are complicating the math. No place in U.S. can you rent a small one bedroom apartment while working and living on minimum wages. Nurses are leaving the labor pool since cost of childcare is so high now, that it does not make financial sense to work and pay for childcare. For women, the math is even worse than for men.

Many large employers have realized that they have no choice but to increase wages. Walmart, Starbucks, Amazon and others that use to count on minimum wages for their employees to keep costs down, and retain high profitability have realized that they can no longer do that. Instead of paying $8-$10 an hour, they now realize they need to pay $15-16 an hour to retain employees. Otherwise they will experience a mass exodus from workforce which will hugely affect their bottom line and profitability.

Everywhere you look, you will see “HELP WANTED” signs. In some industries (like hospitality) employers are offering a sign-up bonus, in some cases, as much as $1,000 to recruit new employees. The labor force is now dictating the compensation through demand and supply.

If people cannot live on a minimum wage, and cost of living and childcare is very high, they simply will look for other options, for instance to live with their parents or move out to countryside where living expenses are much cheaper.

Compensation is now the driving force of attracting and retaining good employees. Smarter employers are going even further to stand out with a differentiation of “employee well-being plan”. They are offering support for childcare, healthcare, and training for personal development. They understand that most people are not transitory in work place and are therefore looking for “meaningful career”.

Inflation

Demand for increased wages – coupled with supply chain issues – have led to higher prices in just about every industry and market sector. The wage increases are here to stay, and won’t be reduced at some point in the future when market stability is achieved.

But inflation will come down at some point in the coming years. But there are challenges that may force inflation not to return to the levels we have seen for 2010-2018, and these include transportation/fuel costs, affordable housing, affordable childcare, and of course competitive workforce wages. Among these the highest cost to an employee (which affects employers), is affordable housing.

Workers obviously cannot stay in a job if they cannot afford a place to live. The nation has a shortage of 1.2 million housing units. Prior to COVID, U.S. had a shortage of housing around half a million per year, now it has more than doubled and the situation got critical to exacerbated by the pandemic since construction companies were not building for an extended period of time.

Check Your Mortgage Rates

Mortgage rates have been near record lows in the last few years, but Federal Reserve has already indicated that they will increase rates, may be as much as 5 times in the next 2 years. With property prices going up an unprecedented 20% per year in parts of the country during a pandemic, even a small decrease in your mortgage interest rate can save you a lot of money over the lifetime of your mortgage. So, check your current interest rates and see if there is a possibility to reduce it, if at all possible. (If you are on an adjustable-rate mortgage, check for how much longer your rate is locked, or see if you can refinance and get a fixed mortgage.

Extending your mortgage to a new 30-year mortgage could lower your payments although make sure that the math really adds up and the fees/cost makes sense. Consider your options carefully, it’s almost always best to consult a financial advisor.

Personal wealth-protection and investment for business owners

Almost every few months, we hear of a new variant of Covid-19 and this has taken a toll on investors’ confidence. Add to this, inflation, supply chain problems, hire wages, and increase in interest rates. This puts quite a bit of pressure on most business owners when it comes to their personal wealth-protection and investments. Not only is their business under pressure, now it seems, so is there retirement funds, wealth-protection, inflationary threats, and market uncertainties.

What are the safe and smart investments today? Is it (FDIC)-insured high-yield savings accounts, or Certificates of Deposits (with up to 2 years locked higher rates), or gold for protection against devaluation of currency, or U.S. Treasury Bonds, or Series/Savings Bonds (some with better rates than many high-yield savings accounts), or corporate bonds, or real estate investment, preferred stocks, IPOs, or digital assets and/or Crypto. All of these possibilities need to be analyzed carefully with your financial advisor to make sure you are making smart decisions for your wealth-protection and your retirement plan.

There are no completely risk-free investments that protect you from every possible scenario, even the safe investment strategies that I just listed above. The smartest thing to do is consider your own individual needs and put together a portfolio that offers sufficient stability while still allowing you to take advantage of growth over time. You can consult with your financial consultant and discuss asset allocation with financial goals based on your preferred risk appetite, explore a balanced advantage fund (BAF), may be top-up health insurance plan, and have an adequate liquid fund strategy to cover emergencies.

All of these together will help alleviate some of the challenges when addressing business ownership strategies during hyperinflation, supply chain issues, and rising interest rate.

This is indeed going to be a roller coaster year. Buckle up.

Planning with smart contingencies is key. Good luck.